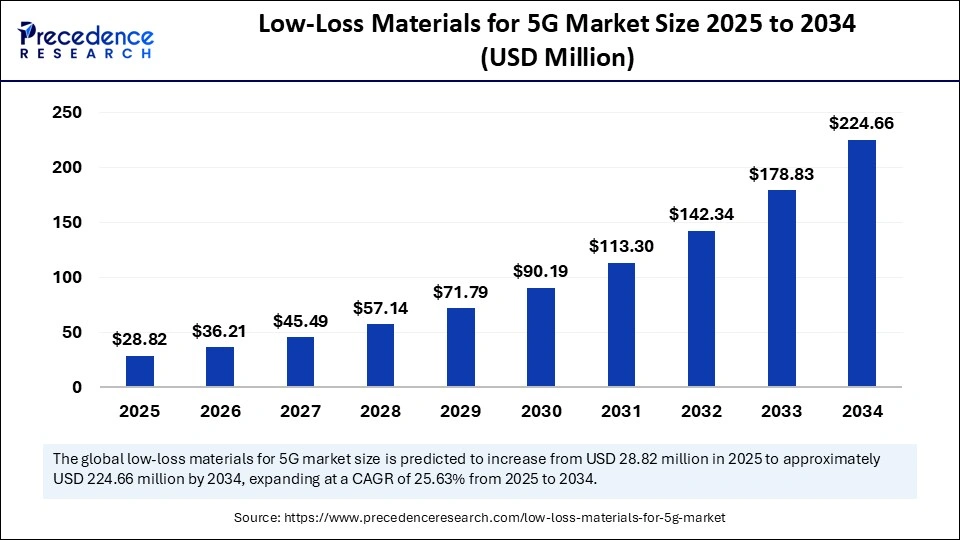

The rapid deployment of 5G technology is driving unprecedented demand for advanced low-loss materials essential to ensure high-speed, low-latency communication with minimal signal loss. Valued at USD 28.82 million in 2025, the global low-loss materials for 5G market is forecasted to surge to USD 224.66 million by 2034, growing at a CAGR of 25.63%.

This growth is fueled by expanding 5G infrastructure, increasing use of high-frequency components in smartphones and IoT devices, and innovations in material science enhancing device miniaturization and performance.

Low-Loss Materials for 5G Market Key Insights

-

The Asia Pacific region dominated with a 39.4% market share in 2024, led by China, Japan, and South Korea’s massive 5G deployments.

-

Polytetrafluoroethylene (PTFE) held the largest share among materials at 42.3% due to its excellent dielectric and thermal properties.

-

Sheets & laminates accounted for the highest product form share at 50.4%, being essential in PCBs and antennas.

-

Antennas and radomes represented the largest application segment with 44.4% market control.

-

Sub-6 GHz frequency range commanded 72.8% market dominance, reflecting widespread deployment compared to mmWave.

-

Base stations captured the largest end-use segment share at 40.5%.

-

Key companies include DuPont, Mitsubishi Chemical, Rogers Corporation, and Panasonic, investing heavily in R&D and advanced materials innovation.

What Role Does AI Play in Advancing Low-Loss Materials for 5G?

Artificial intelligence is a transformative force accelerating the research and development of low-loss materials. AI enables predictive modeling and simulations to design polymers and composites with precise dielectric characteristics and thermal stability, optimizing performance for 5G applications while cutting development costs.

In manufacturing, AI enhances real-time defect detection and automation, ensuring consistent quality in complex material production. Furthermore, AI-assisted design tools facilitate the creation of miniaturized, high-frequency antennas and substrates essential for next-generation communication devices.

How is AI Innovation Impacting 5G Ecosystem Material Development?

By integrating AI into material R&D, manufacturers can rapidly prototype and scale new low-dk (dielectric constant) and low-df (dissipation factor) composites tailored for mmWave and Sub-6 GHz bands. This accelerates the rollout of energy-efficient, high-performance components like RF modules and PCBs while supporting sustainable production practices.

AI-driven advances in materials also underpin improved signal fidelity, device miniaturization, and thermal control, critical for expanding 5G networks across dense urban and remote regions.

What Are the Key Market Growth Factors?

-

Expanding 5G infrastructure globally, especially in Asia Pacific and North America, demands materials that maintain signal integrity at high operating frequencies.

-

Miniaturization trends in smartphones, wearable devices, and IoT modules increase requirement for flexible and lightweight low-loss materials like liquid crystal polymers (LCP).

-

Advances in polymer and ceramic composites improve thermal management and reduce electromagnetic interference (EMI), boosting overall system reliability.

-

Rising adoption of mmWave frequencies to support ultra-high-speed data transmission in smart cities and autonomous systems expands material application scope.

-

Government initiatives and funding support development of next-gen communication infrastructure investing in novel substrate and laminate technologies.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 28.82 Million |

| Market Size in 2026 | USD 36.21 Million |

| Market Size by 2034 | USD 224.66 Million |

| Market Growth Rate from 2025 to 2034 | CAGR of 25.63% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | North Ameirca |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Material Type, Product Form, Application, Frequency Range, End Use, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

What Opportunities and Trends Are Emerging in the Low-Loss Materials for 5G Market?

How are new material types shaping the future of 5G devices?

Liquid crystal polymers and ceramic composites are gaining rapid adoption due to their stability at mmWave frequencies and excellent mechanical properties, enabling flexible and foldable antennas.

What impact does the Asia Pacific region have on market dynamics?

Asia Pacific remains a hub for innovation and production, propelled by strong government policies and partnerships fueling 5G base station deployment and smart city projects.

How are startups influencing market innovation?

Emerging companies focused on nano-ceramics, advanced polymers, and sustainable substrates are introducing cutting-edge, miniaturized solutions that challenge traditional material suppliers.

Which application areas hold the most promise?

Base stations and antennas continue to dominate, but growing automotive V2X communication and consumer electronics markets present significant growth potential.

How Does Regional and Segmentation Analysis Inform Market Strategies?

-

Asia Pacific leads with 39.4% of the market share, driven by China’s dominant manufacturing and infrastructure investments, supported by government policies like Made in China 2025.

-

North America is the fastest-growing region, focusing heavily on mmWave deployment and smart infrastructure, with key players such as Rogers Corporation and DuPont investing in innovation.

-

Europe focuses on sustainable, energy-efficient low-loss materials, driven by increased 5G infrastructure and digital transformation efforts.

-

Among material types, PTFE remains dominant for its dielectric performance, while LCP shows rapid growth for flexible electronics.

-

Sheets & laminates are essential components in base station and PCB manufacturing, representing over half the market share.

-

The largest applications are antennas & radomes, RF modules, and PCBs, supporting a variety of end uses from base stations to automotive communication systems.

What Are the Latest Breakthroughs and Leading Companies’ Contributions?

Several industry leaders are pioneering novel low-loss materials and technologies:

-

DuPont offers high-frequency circuit materials like RO3000 and Pyralux laminates, optimized for 5G antennas and base stations.

-

Mitsubishi Chemical manufactures fluoropolymer and ceramic-based materials critical for antennas and high-frequency PCBs.

-

Rogers Corporation develops PTFE laminates tailored for 5G infrastructure demanding excellent dielectric stability.

-

Shin-Etsu Chemical advanced Qromis Substrate Technology for GaN power devices, with implications for efficient 5G components.

-

Doosan Corporation Electro-Materials launched new 5G connectivity solutions leveraging beamforming technology for scalable small cells.

What Challenges and Cost Pressures Does the Market Face?

-

High development and production costs for advanced polymer and ceramic composites limit widespread adoption, especially in emerging markets.

-

Technical challenges remain in achieving ultra-low signal loss while maintaining flexibility, thermal stability, and environmental durability.

-

Supply chain constraints for raw materials such as fluoropolymers may impact production scalability.

-

Balancing miniaturization with signal integrity requires continual R&D investments, increasing overall costs.

-

Regulatory and environmental compliance for new materials add complexity and potential cost burdens.

Case Study: Accelerating 5G Deployment Through Material Innovation

A leading telecom equipment manufacturer collaborated with a low-loss material supplier to develop PTFE-based sheets with enhanced thermal dissipation for 5G mmWave antennas. This innovation reduced signal attenuation by 15% while enabling a 20% reduction in antenna weight, facilitating easier installation and improved network coverage in urban environments. The partnership leveraged AI-driven simulations to optimize material formulation, speeding up time-to-market and cutting R&D expenses significantly.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7134

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026