A New Era Dawns for Mental Healthcare as Advances in Generative AI Accelerate Personalized, Accessible Mind Health Solutions Worldwide.

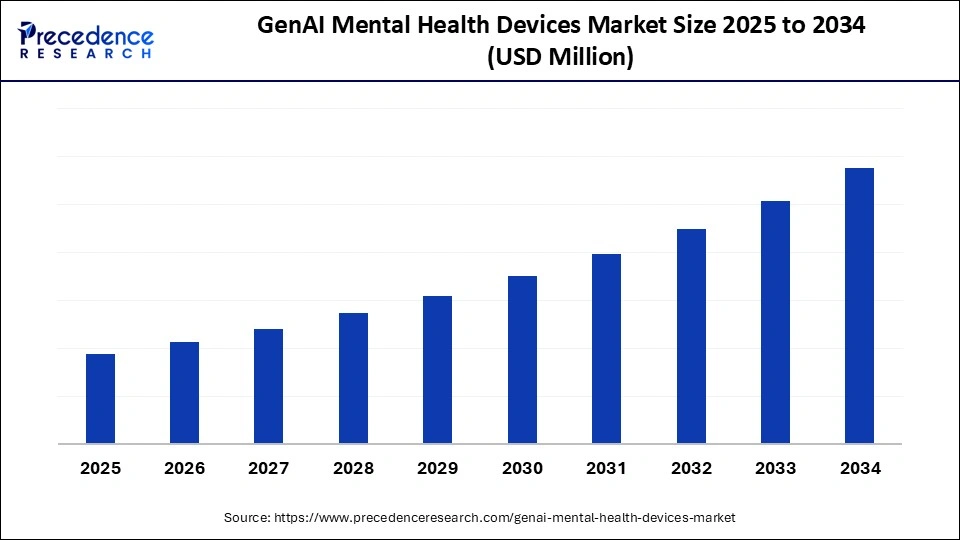

The global GenAI mental health devices market is on a transformative growth trajectory, projected to surge from its base in 2024 to unprecedented levels by 2034, riding on a robust CAGR as digital therapeutics and AI-guided support become the new standard in mental wellness.

The proliferation of AI-powered wearables, diagnostic tools, and app-integrated devices is fundamentally changing how emotional health is monitored, diagnosed, and supported across consumer, clinical, and workplace environments. Rising mental health awareness, the quest for personalized support, and broader regulatory acceptance are catalyzing adoption, especially in North America and Asia Pacific—the fastest growing region on the horizon.

GenAI Mental Health Devices Market Key Insights

-

North America led the GenAI mental health devices market with a 38% share in 2024.

-

Asia Pacific is forecasted to grow at the fastest CAGR through 2034.

-

Wearable devices constitute 35% of the market, providing always-on emotional support and remote monitoring.

-

The mobile & app-integrated segment is the fastest-growing, as demand soars for AI-guided, stigma-free support.

-

Adults (18-60) represent approximately 60% of users, seeking productivity and stress management.

-

Retail stores hold a 35% market share, but online platforms are catching up swiftly with new subscription models.

-

AI-powered cognitive behavioral therapy (CBT) devices command 40% of the market, delivering evidence-based, scalable therapy.

-

Key players: Lyra Health, Quartet Health, Happify Health, Flow Neuroscience, BrainsWay, Empatica, Muse (InteraXon), Neurable, BioBeats.

GenAI Mental Health Devices Market Revenue Breakdown

| Segment | Market Share 2024 (%) |

|---|---|

| Wearable Devices | 35 |

| Mobile & App-Integrated Devices | 25 |

| Portable Diagnostic Devices | 15 |

| VR/AR Therapeutic Devices | 10 |

| Stationary Clinical Devices | 8 |

| Other Devices & Accessories | 7 |

| End User | Market Share (%) |

|---|---|

| Adults (18–60) | 60 |

| Seniors (60+) | 15 |

| Adolescents/Teens | 12 |

| Children (<12) | 8 |

Generative AI is rewriting the rules of mental health support by enabling real-time, deeply personalized interventions. These devices, powered by advanced algorithms and large language models, can emulate empathetic dialogues, detect subtle mood shifts, and deliver dynamic, evidence-based therapy that feels authentic and user-centric. By integrating sensor data—heart rate, sleep, neural signals—with proactive coaching and smart nudging, GenAI solutions bridge the care gap, especially where human resources are scarce or stigma is high.

Cloud-native architectures, multilingual models, and privacy-preserving features propel innovation, ensuring these devices work seamlessly across diverse populations. As regulatory frameworks mature and public trust grows, collaborative models between clinicians and AI systems are becoming normalized, further embedding GenAI tools into mainstream care pathways—from home apps to hospital systems and nationwide tele-mental health programs.

Why Is Demand Surging for GenAI Devices?

What factors are turning AI-driven devices into must-have tools for mental health?

-

Growing shortages of mental health professionals have left millions underserved—GenAI devices offer instant, scalable support.

-

The rise in clinical depression, anxiety, and stress underpins demand for always-available, stigma-free tools.

-

Increased comfort with digital health, driven by pandemic-era telemedicine, means consumers expect personalized, app-based solutions.

What Opportunities and Trends Are Driving Market Growth?

How are market opportunities unfolding for innovators and investors?

Can AI replace traditional therapy?

GenAI isn’t replacing clinicians—it’s complementing them by offering preliminary triage, continuous engagement, and evidence-based behavioral nudges, all at lower cost.

Is the enterprise ready?

Corporate wellness programs are emerging as a major frontier, using GenAI wearables and dashboards to boost workforce resilience and productivity, while supporting hybrid and remote workforces.

Are we seeing truly accessible mental care?

Multilingual, culturally adaptive platforms are opening access in regions with high unmet need, such as India’s Tele-MANAS initiative and Latin America’s expanding digital care networks.

What Are the Latest Breakthroughs from Industry Leaders?

Which advances are setting the pace in 2025 and beyond?

-

In May 2025, Israeli startup Mentaily raised $3 million to develop its LIV AI diagnostic platform, backed by Microsoft and KPMG.

-

Cedars Sinai debuted “Xaia,” an immersive AI therapy app for Apple Vision Pro, blending spatial computing and personalized avatars for therapy.

-

Healthcare Triangle Inc. launched QuantumNexis, with strategic acquisitions to build a generative AI-powered platform for healthcare data.

Top Companies:

-

Lyra Health, Quartet Health, Happify Health, Flow Neuroscience, BrainsWay, Empatica, Muse (InteraXon), Neurable, BioBeats, Woebot, Wysa, Koa Health, Headspace, Ginger, Talkspace, BetterHelp, Pear, Mindstrong, Limbic AI, Spring Health.

GenAI Mental Health Devices Market Regional Analysis

-

North America: With 38% share, North America is leading due to robust digital infrastructure, regulatory clarity, and heavy investment in pilot programs and reimbursement pathways.

-

Asia Pacific: Fastest CAGR, propelled by high smartphone penetration, unmet needs, and government initiatives (notably in India and China) fostering digital mental health adoption.

-

Europe: Strong on data protection and regulatory frameworks, with Germany and the Nordics emerging as leaders in digital therapy adoption.

-

Latin America: Growth catalyzed by telehealth expansion and government-sponsored digital care networks, especially in Brazil.

-

Middle East & Africa: Tailored adoption in urban clusters, aided by rising awareness and mobile-first health strategies.

Segment Analysis

-

Product Type: Wearables dominate (35%), with strong growth for mobile/app-integrated and diagnostic devices.

-

Deployment: Home/personal use is primary (50%), but workplaces are the fastest-rising context.

-

Distribution: Physical retail still leads, but online/e-commerce fast gaining traction.

-

Technology: CBT-driven devices are #1; neurofeedback/stimulation is the fastest climber.

-

End User: Adults are the largest group, but adoption is accelerating fast among seniors and adolescents.

Case Study – India’s Tele-MANAS Program

India’s Tele-MANAS national tele-mental health program, leveraging AI for 24×7 support, exemplifies the power of scalable, culturally adaptable GenAI platforms to reach rural and urban users with stigma-free, personalized help. High smartphone access and strong government-university partnership have made India a testing ground for the world’s next-generation mental health tools.

What Are the Main Challenges and Cost Pressures?

-

Data Privacy and Trust: As sensitive personal data is processed by AI, developers must comply with HIPAA, GDPR, and country-specific frameworks—a non-trivial investment.

-

Cost of Innovation: Clinical validation and regulatory approvals can be costly, especially as authorities demand more robust trial data for safety and efficacy.

-

User Engagement: Breakthroughs in AI need to be matched by intuitive design and trust-building to ensure sustained adoption and adherence.

-

Integration: Seamless cooperation between AI tools and clinician workflows remains a pain point, particularly in legacy health systems.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7130

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026