Global Wind Turbine Industry Expands at 7.69% CAGR as Governments, Utilities, and Corporations Invest Heavily in Onshore and Offshore Wind Projects

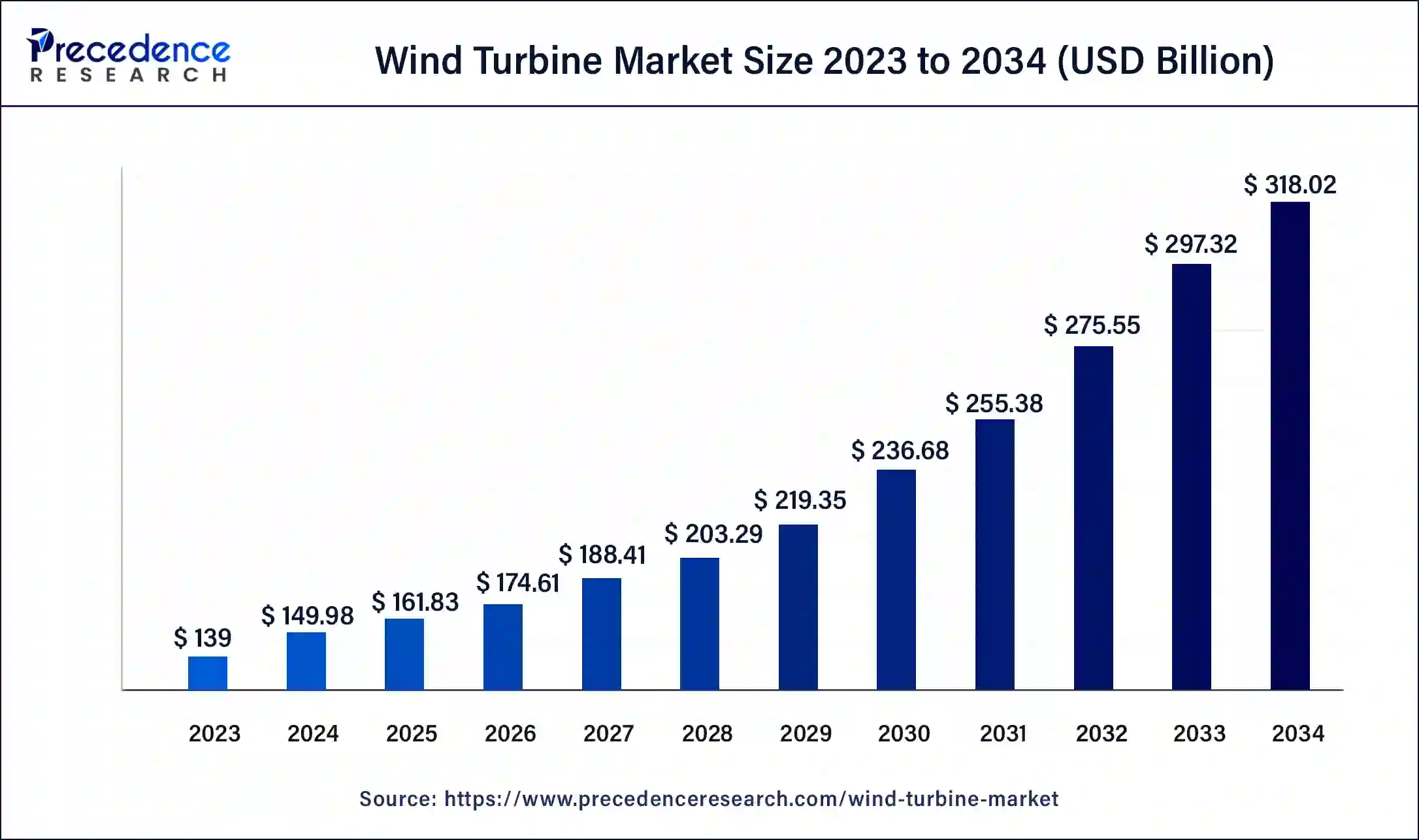

The global wind turbine market size surpassed USD 161.83 billion in 2025 and is projected to rise from USD 174.61 billion in 2026 to approximately USD 339.43 billion by 2035, registering a CAGR of 7.69% during the forecast period from 2026 to 2035. The market is witnessing robust expansion due to rising investments in renewable energy infrastructure, increasing concerns regarding climate change, favorable government incentives, and growing efforts to reduce dependence on fossil-fuel-based power generation.

Wind energy has emerged as one of the most cost-effective and sustainable sources of electricity generation worldwide. As countries race to achieve carbon neutrality targets and comply with international climate agreements, wind turbine deployment across both onshore and offshore installations continues to accelerate. Technological innovations in turbine design, blade efficiency, digital monitoring systems, and offshore engineering are further strengthening the market outlook.

Wind Turbine Market Key Points

• The global wind turbine market was valued at USD 161.83 billion in 2025 and is forecasted to reach USD 339.43 billion by 2035.

• The market is expected to expand at a healthy CAGR of 7.69% between 2026 and 2035.

• Asia Pacific accounted for the largest market share of 59% in 2025 due to strong installations in China and India.

• The onshore installation segment maintained its dominance owing to lower deployment costs and easier grid integration.

• Rotor blades emerged as the leading component segment because of growing demand for high-efficiency turbines.

• Utility-scale projects represented the largest application category supported by government-backed renewable energy initiatives.

• China remains the world’s largest wind power producer and continues to lead offshore turbine installations.

• Companies including Vestas, Siemens Gamesa, GE Renewable Energy, Suzlon Energy, Nordex, Shanghai Electric, and Goldwind continue to shape global market competition.

Wind Turbine Market Revenue Outlook

| Year | Market Size (USD Billion) |

|---|---|

| 2025 | 161.83 |

| 2026 | 174.61 |

| 2035 | 339.43 |

Asia Pacific Revenue Forecast

| Year | Market Size (USD Billion) |

| 2025 | 95.48 |

| 2035 | 202.39 |

How is Artificial Intelligence Transforming the Wind Turbine Industry?

Artificial intelligence is rapidly becoming a critical enabler of operational efficiency in wind energy projects. AI-powered predictive maintenance systems can analyze turbine performance data in real time, identify anomalies before failures occur, and significantly reduce downtime. This capability helps operators maximize electricity generation while lowering maintenance expenses.

In addition, AI-driven weather forecasting models are improving wind resource assessment and energy output prediction. Advanced analytics platforms help utilities optimize grid integration, energy storage management, and turbine placement strategies. As digitalization becomes central to renewable energy infrastructure, AI is expected to play a major role in improving turbine lifespan, operational reliability, and investment returns.

Why is Demand for Wind Turbines Increasing Worldwide?

The global energy transition is creating unprecedented demand for renewable power generation technologies. Governments across developed and developing economies are implementing aggressive renewable energy targets to reduce greenhouse gas emissions and strengthen energy security.

Tax credits, subsidies, renewable portfolio standards, and green financing initiatives have encouraged both public and private investments in wind power projects. The growing mismatch between electricity demand and conventional power generation capacity is also encouraging nations to accelerate wind energy deployment.

Another major growth catalyst is the decline in the cost of wind-generated electricity. Larger turbines, longer blades, advanced materials, and digital control systems have improved efficiency while lowering lifecycle costs. Offshore wind projects are particularly benefiting from these technological advancements as developers install larger turbines capable of generating substantially more power.

Can Offshore Wind Become the Next Major Growth Engine?

Offshore wind energy is emerging as one of the fastest-growing segments within the renewable energy sector.

Offshore projects benefit from stronger and more consistent wind speeds compared to onshore installations. This allows developers to generate significantly higher electricity output while reducing land-use challenges. Furthermore, floating wind turbine technologies are opening new opportunities in deeper waters where conventional fixed-bottom installations are not feasible.

Many governments across Europe, Asia Pacific, and North America are launching offshore wind auctions and investment programs, creating a strong pipeline of future projects.

What Emerging Trends Are Reshaping the Wind Turbine Market?

Several transformative trends are shaping the future of the industry:

Development of Ultra-Large Turbines

Manufacturers are increasingly developing larger turbines with higher power ratings and longer blades to maximize energy production.

Expansion of Offshore Wind Farms

Countries worldwide are investing heavily in offshore wind infrastructure to achieve renewable energy targets and improve energy security.

Sustainable Turbine Manufacturing

Companies are introducing recyclable blades and low-carbon manufacturing practices to align with global ESG commitments.

AI-Driven Smart Turbines

Advanced sensors, digital twins, machine learning algorithms, and predictive maintenance systems are improving turbine performance and reducing operational costs.

Integration with Energy Storage Systems

Battery storage and hydrogen production systems are increasingly being integrated with wind farms to address intermittency challenges.

Expert Perspective

According to Precedence Research, Principal Consultant,

“The wind turbine industry is entering a transformative decade driven by ambitious decarbonization goals, technological breakthroughs, and expanding offshore deployments. Manufacturers that successfully integrate digital intelligence, advanced materials, and sustainable production practices will gain a significant competitive advantage in the evolving renewable energy landscape.”

Wind Turbine Market Segment Analysis

Axis Analysis

Based on axis type, the vertical-axis segment is expected to dominate the global wind turbine market and witness the fastest growth throughout the forecast period. The growth of this segment is primarily attributed to its ability to deliver high operational efficiency while maintaining relatively lower installation and maintenance costs, making it an attractive option for various wind energy projects.

Installation Analysis

By installation type, the wind turbine market is segmented into onshore and offshore installations. The onshore segment held the largest market share in 2024 and is anticipated to maintain its dominance during the forecast period. This growth is driven by the increasing preference for onshore wind farms due to their lower development costs, easier accessibility, and widespread deployment across regions.

Meanwhile, the offshore segment is projected to experience significant growth over the coming years. Rising investments in renewable energy infrastructure and the growing emphasis on clean energy generation are encouraging the adoption of offshore wind projects. Offshore wind turbines offer several advantages, including higher energy output resulting from stronger and more consistent wind speeds, as well as improved operational efficiency.

Components Analysis

Based on components, the market is categorized into rotor blades, generators, gearboxes, nacelles, and others. The rotor blade segment accounted for the largest market share in 2024 and is expected to continue its growth trajectory throughout the forecast period. The increasing demand for electricity, coupled with rapid industrialization and expansion of power generation infrastructure, is driving the adoption of advanced rotor blade technologies to enhance turbine performance and energy efficiency.

Application Analysis

In terms of application, the wind turbine market serves utility, industrial, commercial, and residential sectors. The utility segment dominated the market in 2024 and is expected to retain its leading position during the forecast period. This dominance is supported by government initiatives, favorable regulatory policies, and increasing investments in large-scale renewable energy projects aimed at achieving sustainability and reducing carbon emissions.

The residential segment is also expected to witness notable growth over the forecast period. Factors such as rapid urbanization, growing awareness of renewable energy, and increasing adoption of decentralized power generation systems are contributing to the rising demand for residential wind energy solutions.

Wind Turbine Market Regional Analysis

Asia Pacific accounted for approximately 59% of global revenue in 2025, making it the largest regional market.

The region benefits from strong manufacturing capabilities, expanding electricity demand, favorable government policies, and substantial renewable energy investments. China remains the dominant force, while India, Japan, and South Korea continue expanding their wind energy capacities.

China’s aggressive renewable energy targets, large-scale offshore developments, and strong domestic manufacturing ecosystem have positioned the country as the global leader in wind turbine deployment.

In May 2025, China unveiled the world’s largest offshore wind turbine featuring a hub height of 185 meters and a capacity of 26 MW, capable of generating approximately 100 million kWh annually.

North America remains a key contributor to global wind energy expansion.

The United States leads the regional market due to strong policy support, federal tax incentives, and significant investments enabled by the Inflation Reduction Act. States such as Texas, Iowa, and Oklahoma continue to host some of the largest wind energy projects globally.

The region is also experiencing growing investments in offshore wind infrastructure and next-generation turbine technologies.

Europe continues to lead technological innovation in wind turbine manufacturing and offshore wind deployment.

Countries such as Germany, the United Kingdom, Denmark, and Spain maintain ambitious net-zero goals and strong renewable energy frameworks. Mature supply chains and extensive offshore expertise further strengthen Europe’s competitive position.

Latin America is rapidly emerging as an attractive destination for renewable energy investments.

Countries including Brazil, Chile, and Mexico are expanding wind farm development programs to address growing electricity demand while supporting sustainable economic growth. Government-backed renewable energy auctions and improving grid infrastructure are creating favorable market conditions.

Wind Turbine Market Value Chain Analysis

The wind turbine industry’s value chain consists of three primary stages:

Raw Material and Component Manufacturing

This stage includes production of steel towers, fiberglass blades, rare-earth materials, generators, gearboxes, control systems, and electronic components.

Turbine Assembly and Installation

Major manufacturers assemble turbine systems and oversee transportation, site preparation, construction, and commissioning activities.

Operations and Maintenance

Long-term performance optimization involves predictive maintenance, remote monitoring, digital analytics, and turbine servicing to maximize operational efficiency.

Recent Industry Developments

ZF Wind Power Launches India’s Largest Test Rig

In May 2025, ZF Wind Power introduced a 13.2 MW test rig in Coimbatore designed to validate next-generation gearboxes and powertrains under extreme operating conditions.

Senvion India Introduces New Wind Turbine Platform

Senvion India launched its 3.1 M130 wind turbine platform designed specifically to maximize annual energy production under Indian wind conditions.

Haventus and Sarens Advance Floating Offshore Wind

The companies introduced a cost-effective solution aimed at accelerating floating offshore wind turbine deployment while reducing installation expenses.

Enel Launches WinDesign Initiative

Enel unveiled WinDesign, a project focused on improving the visual integration of wind turbines into surrounding landscapes to support broader renewable energy adoption.

GE Renewable Energy Expands Indian Projects

GE Renewable Energy announced the supply of 42 units of its 2.7-132 onshore wind turbines for projects across Gujarat and Karnataka.

Leading Companies in the Wind Turbine Market

GE Vernova (formerly General Electric Company)

GE Vernova accounted for an estimated 6.4% share of the global wind turbine market revenue in 2025, generating approximately USD 10.9 billion from its wind business. The company offers a broad portfolio of onshore wind turbines, including its Cypress platform, along with grid integration solutions, digital asset monitoring technologies, and long-term operations and maintenance services.

Vestas Wind Systems A/S

Vestas Wind Systems A/S held an estimated 10.2% revenue share of the global wind turbine market in 2025, representing around USD 17.4 billion in wind turbine-related revenue. The company provides a comprehensive range of onshore and offshore wind turbines, including the EnVentus and V236 platforms, complemented by project development, service agreements, and lifecycle management solutions.

Nordex SE

Nordex SE captured approximately 4.7% of the global wind turbine market revenue in 2025, with estimated wind business revenue of USD 8.0 billion. Its offerings primarily include onshore wind turbines based on the Delta4000 platform, turnkey wind farm solutions, and extensive maintenance and operational support services.

Suzlon Energy Limited

Suzlon Energy Limited represented an estimated 1.7% share of the global wind turbine market revenue in 2025, generating around USD 2.9 billion from its wind operations. The company offers wind turbine generators such as the S144 and S133 series, alongside end-to-end wind farm development, project execution, and operations and maintenance services.

Siemens Gamesa Renewable Energy S.A.

Siemens Gamesa Renewable Energy S.A. accounted for approximately 9.1% of the global wind turbine market revenue in 2025, equivalent to nearly USD 15.6 billion. The company’s portfolio includes advanced offshore wind turbines, such as the SG 14-236 DD series, onshore turbine solutions, digital diagnostics, and comprehensive lifecycle service offerings.

China State Shipbuilding Corporation (CSIC) – Haizhuang Windpower

CSIC, through its Haizhuang Windpower division, held an estimated 2.4% share of the global wind turbine market revenue in 2025, generating approximately USD 4.1 billion. The company provides large-capacity onshore and offshore wind turbines, as well as integrated wind farm development and engineering solutions.

Shanghai Electric

Shanghai Electric accounted for an estimated 3.6% of global wind turbine market revenue in 2025, with wind-related revenue of approximately USD 6.2 billion. Its offerings include onshore and offshore wind turbine platforms, particularly high-capacity offshore models ranging from 8 MW to 16 MW, supported by smart operations and maintenance services.

Windey Energy Technology Group Co., Ltd.

Windey Energy Technology Group Co., Ltd. captured an estimated 4.2% share of the global wind turbine market revenue in 2025, generating roughly USD 7.1 billion from its wind business. The company offers a range of onshore and offshore wind turbines, modular high-capacity turbine platforms, wind farm engineering services, and lifecycle support solutions.

Wind Turbine Market Segmentation

By Axis

- Vertical

- Horizontal

By Installation

- Offshore

- Onshore

By Components

- Rotor Blade

- Generator

- Gearbox

- Nacelle

By Application

- Residential

- Utility

- Industrial

- Commercial

By Capacity

- Small

- Medium

- Large

By Connectivity

- Grid Connected

- Stand Alone

By Rating

- Less than 100 kW

- 100 kW to 250 kW

- Above 250 kW to 500 kW

- Above 500 kW to 1 MW

- 1 MW to 2 MW

- Above 2 MW

Also Read: Solar Photovoltaic Market Size to Surpass USD 484.85 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/1722

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- 360-Degree Camera Market Set for Explosive Growth, Reaching USD 27.21 Billion by 2035 as AI-Powered Imaging and Immersive Content Reshape Digital Experiences - June 30, 2026

- Automotive Transmission Market Size Forecasted to Reach USD 287.55 Billion by 2035 as Demand for Fuel-Efficient and Electrified Vehicles Accelerates - June 29, 2026

- From Memory Enhancement to Alzheimer’s Care: Brain Health Supplements and Therapeutics Market Set for Strong Growth Through 2035 - June 25, 2026