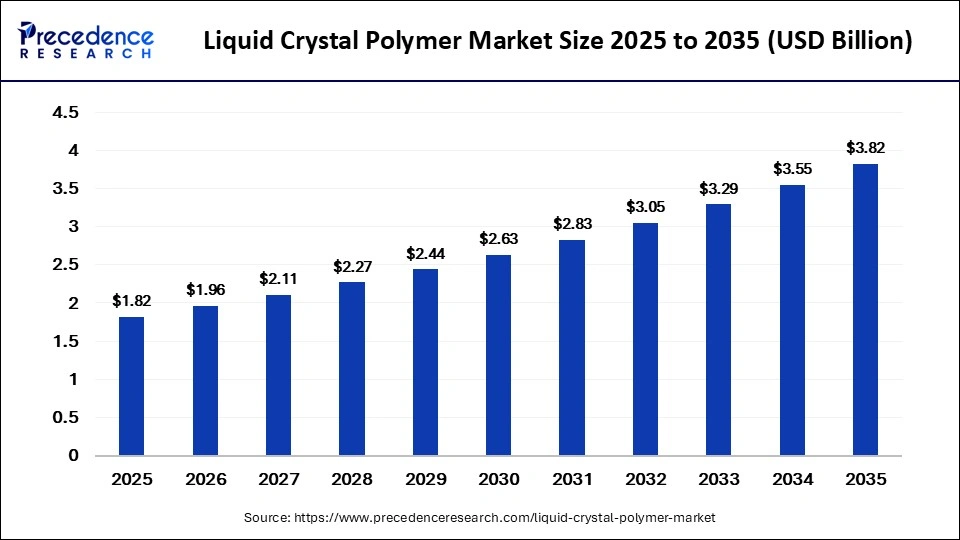

The global liquid crystal polymer market is projected to grow from USD 1.96 billion in 2026 to USD 3.82 billion by 2035, driven by rising demand for miniaturized electronics, 5G infrastructure, aerospace applications, and advanced semiconductor technologies.

Read Also: AI in Product Lifecycle Management Market

What is Liquid Crystal Polymer?

Liquid Crystal Polymer (LCP) is a high-performance thermoplastic that exhibits liquid crystalline behavior when heated. Unlike conventional plastics, LCP offers exceptional mechanical strength, dimensional stability, chemical resistance, low moisture absorption, and excellent electrical properties.

These characteristics make LCP an ideal material for applications requiring precision, durability, and performance under extreme conditions.

Today, LCP is widely used in:

- Electrical connectors

- Semiconductor packaging

- Automotive electronics

- Medical devices

- Aerospace communication systems

- 5G antennas

- Flexible electronic circuits

Its ability to maintain structural integrity in demanding environments positions it as one of the most advanced engineering plastics available.

Key Market Highlights

- Asia Pacific dominated the market with a 46% share in 2025

- Thermotropic liquid crystal polymers accounted for 91% of market revenue

- Resin remained the leading form segment with 62% market share

- Electrical & electronics applications contributed 48% of total revenue

- Electronics & semiconductor industry captured 52% share

- Films segment is expected to grow at the fastest CAGR of 9.3%

- Asia Pacific is forecast to expand at the highest CAGR of 9.2% through 2035

Why Demand for Liquid Crystal Polymers is Rising

Miniaturization of Electronics

One of the biggest growth drivers for the liquid crystal polymer market is the ongoing trend toward smaller, lighter, and more powerful electronic devices.

LCP materials provide:

- Superior dimensional stability

- Excellent dielectric properties

- High heat resistance

- Low moisture absorption

These properties make them ideal for manufacturing compact connectors, sensors, chip carriers, and semiconductor components used in smartphones, wearables, and advanced computing devices.

Expansion of 5G Infrastructure

The global rollout of 5G networks is creating substantial demand for advanced materials capable of supporting high-frequency signal transmission.

LCP films have emerged as a preferred material because they offer:

- Low dielectric constant

- Excellent signal integrity

- High-frequency performance

- Lightweight design

As telecommunications infrastructure expands worldwide, demand for LCP-based components is expected to increase significantly.

Growth in Automotive Electronics

Modern vehicles increasingly rely on sophisticated electronic systems for safety, connectivity, and autonomous driving functions.

Liquid crystal polymers are widely used in:

- Radar systems

- Sensor housings

- Connectors

- Battery management systems

- Electric vehicle components

Their heat resistance and electrical performance make them ideal for automotive applications where reliability is critical.

How Artificial Intelligence is Influencing the Market

Artificial Intelligence is playing a growing role in polymer science and materials engineering.

Researchers are leveraging AI technologies to:

- Predict polymer behavior

- Optimize material properties

- Accelerate product development

- Improve manufacturing efficiency

- Enhance performance modeling

Advanced machine learning algorithms such as convolutional neural networks (CNNs) and support vector machines (SVMs) are increasingly being used to study liquid crystal materials and develop next-generation polymer formulations.

Emerging Market Trends

Rising Adoption in Aerospace Applications

The aerospace industry is increasingly utilizing LCP films in communication systems and RF antennas.

Benefits include:

- Lightweight construction

- High-frequency signal transmission

- Thermal stability

- Reduced system weight

These advantages are making LCP a critical material in modern aerospace communication technologies.

Growing Use in Semiconductor Packaging

Semiconductor manufacturers are increasingly incorporating liquid crystal polymers into advanced packaging solutions.

Their superior electrical insulation and dimensional stability help improve chip performance while supporting the miniaturization trend within the semiconductor industry.

Flexible Electronics Driving Film Demand

LCP films are experiencing strong growth due to increasing adoption in:

- Flexible displays

- Wearable devices

- Advanced communication systems

- High-frequency electronic packaging

The films segment is expected to register the fastest growth rate during the forecast period, supported by the rapid expansion of flexible electronics and 5G technologies.

Market Dynamics

Driver: Expansion of Electronics Manufacturing

The rapid growth of global electronics manufacturing remains the primary factor driving market demand.

Increasing production of:

- Smartphones

- Consumer electronics

- Semiconductor devices

- Communication equipment

continues to generate substantial opportunities for liquid crystal polymer manufacturers.

Restraint: High Material Costs

Despite its advantages, LCP remains significantly more expensive than conventional engineering plastics such as ABS and polyphthalamide.

The higher production and material costs can limit adoption among cost-sensitive manufacturers, particularly in emerging markets.

Opportunity: Advanced Circuit Substrates

The increasing use of multilayer resin substrates in advanced circuit boards presents a major growth opportunity.

LCP-based substrates support:

- High-speed data transmission

- 3D circuit architectures

- Enhanced reliability

- Superior moisture resistance

These capabilities are becoming increasingly valuable in next-generation communication and computing systems.

Segment Analysis

Thermotropic Liquid Crystal Polymer Leads the Market

The thermotropic liquid crystal polymer segment accounted for 91% of market share in 2025.

Its dominance is attributed to widespread use in electronics manufacturing, where precise molding and excellent thermal stability are essential.

Applications include:

- Connectors

- Electronic housings

- Automotive electronics

- Consumer electronics

The segment is expected to maintain leadership throughout the forecast period.

Resin Segment Dominates by Form

Resin represented 62% of total market revenue in 2025.

Its popularity stems from increasing demand for injection-molded electronic components and precision-engineered products.

The segment continues to benefit from advancements in manufacturing technologies and growing demand for heat-resistant materials.

Electrical & Electronics Segment Remains the Largest Application

Electrical and electronics applications accounted for 48% of market share in 2025.

The segment’s growth is driven by:

- Semiconductor expansion

- Consumer electronics production

- Miniaturization trends

- High-frequency communication devices

The sector is expected to remain the primary revenue contributor through 2035.

Regional Insights

Asia Pacific Leads Global Growth

Asia Pacific dominated the market with 46% market share in 2025 and is projected to expand at the fastest CAGR of 9.2%.

Growth is supported by:

- Strong electronics manufacturing base

- Rapid industrialization

- Expansion of automotive production

- Semiconductor investments

Countries such as China, Japan, South Korea, and Taiwan continue to drive regional demand.

China Remains the Largest Regional Contributor

China’s dominance is driven by:

- Massive electronics manufacturing capacity

- Semiconductor industry growth

- Government support for advanced materials

- Rising investments in research and development

Manufacturers continue investing heavily in high-performance polymer technologies to improve product capabilities.

North America Strengthens Semiconductor Demand

North America held approximately 24% market share in 2025.

The region benefits from:

- Advanced semiconductor manufacturing

- 5G infrastructure deployment

- Aerospace innovation

- Medical technology development

The United States remains a key market for high-performance polymers used in next-generation technologies.

Europe Benefits from EV and Aerospace Expansion

Europe accounted for 21% of global revenue in 2025.

Increasing electric vehicle production, aerospace innovation, and regulatory focus on lightweight materials are supporting regional growth.

Germany continues to lead the European market due to strong demand for automotive radar systems and industrial electronics.

Leading Companies in the Liquid Crystal Polymer Market

Major companies operating in the market include:

- Celanese Corporation

- Sumitomo Chemical

- Toray Industries

- Polyplastics Co.

- Solvay

- SABIC

- Kuraray

- RTP Company

- Mitsubishi Engineering-Plastics

- Kingfa Sci. & Tech.

These companies continue investing in advanced polymer research, sustainable manufacturing technologies, and next-generation material innovation.

Conclusion

The liquid crystal polymer market is poised for sustained growth as industries increasingly adopt advanced materials capable of meeting the performance requirements of modern electronics, automotive systems, aerospace applications, and healthcare devices. Driven by 5G deployment, semiconductor innovation, flexible electronics, and AI-assisted materials research, LCP is emerging as a cornerstone material for future high-performance technologies.

With Asia Pacific leading global production and demand, and technological advancements unlocking new applications, the liquid crystal polymer market is expected to remain a critical segment within the advanced materials industry through 2035.

Get Sample Copy: https://www.precedenceresearch.com/sample/8441

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at [email protected]