Soaring Electric Vehicle Adoption and Advanced E-Axle Technologies Power a Double-Digit CAGR Surge

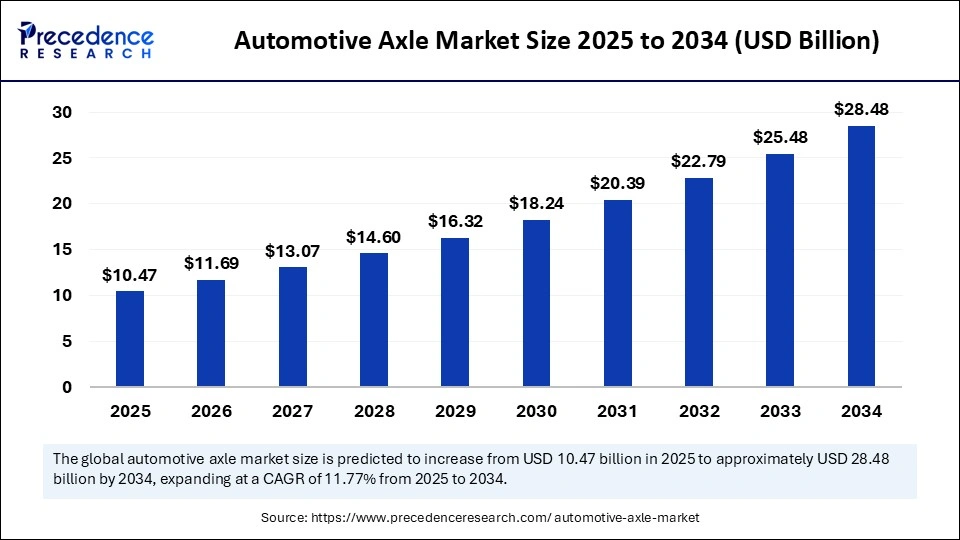

The global automotive axle market is poised for a robust expansion, with its valuation forecasted to leap from $10.47 billion in 2025 to a commanding $28.48 billion by 2034. This impressive growth, at a CAGR of 11.77% over the 2025–2034 period, is firmly driven by breakneck EV adoption, e-axle innovations, infrastructure investments, and the rise of AI-powered manufacturing.

Automotive axles, the core element underpinning every vehicle’s movement and performance, are entering a golden age of innovation. What’s behind this market’s rapid transformation? EV momentum, relentless urbanization, and a relentless push by manufacturers to deliver more intelligent, energy-efficient, and lightweight axle systems.

With global electric vehicle sales soaring by 25% in Q1 2024 and new e-axle architectures redefining drivetrain design, the axle industry is preparing to scale new heights.

Quick Insights: Automotive Axle Market

-

2024 Market Size: $9.37 billion

-

2025 Estimate: $10.47 billion

-

2034 Projection: $28.48 billion

-

CAGR (2025–2034): 11.77%

-

Leading Region: Asia Pacific (50% market share, $4.68B in 2024)

-

Fastest Growth: South America

-

Top Segment by Vehicle Type: Passenger Cars (61% share)

-

Dominant Axle Type: Drive Axle (65% share)

-

Top Material: Steel (73% share)

-

Key Companies: ZF Friedrichshafen AG, Schaeffler Group, BorgWarner Inc., Continental AG

-

OEM Market Share: 70%

| Metric | 2024 Value | 2025 Value | 2034 Value | CAGR (2025–34) |

|---|---|---|---|---|

| Total Market Size | $9.37B | $10.47B | $28.48B | 11.77% |

| Asia Pacific Market Size | $4.68B | — | $14.38B | 11.88% |

What’s Powering Growth?

How Is Surging Electric Vehicle Adoption Transforming the Axle Market?

Key market drivers stem from the global shift toward electric vehicles. In 2024, electric car sales soared past 3 million, a 25% leap, with China alone contributing nearly half a million units and dominating 80% of the worldwide growth.

Major automakers are accelerating the development and integration of e-axles, which integrate motor, power electronics, and transmission in a single lightweight, space-saving module. These modern axle solutions are pivotal in maximizing EV efficiency, extending driving range, and meeting global decarbonization goals.

What Role Does AI Play in the Next-Gen Axle Market?

Artificial intelligence is reshaping axle manufacturing with advanced modeling tools that optimize designs for high-torque, lightweight construction. Real-time machine learning enables manufacturers to spot and correct defects, cut energy usage, and streamline axle production for both fleet and mass-market models.

Segmentation and Regional Insights

Why Does Asia Pacific Dominate the Automotive Axle Arena?

Asia Pacific captured half of the global market in 2024, fueled by explosive vehicle production—over 30 million units in China alone—and breakthroughs in electric mobility from leaders like BYD, Tata Motors, Hyundai, and Toyota. Manufacturers such as Dana Incorporated and ZF Friedrichshafen ramped up regional production to supply both OEM and aftermarket demand, supported by robust government incentives for electrification.

South America is posting the fastest sales gains, with Brazil’s vehicle output up 10% in 2024 and expanded demand in commercial/logistics sectors. Flexible-fuel policies and infrastructure growth across Brazil, Chile, and Colombia feed further axle demand for LCVs and heavy-duty trucks.

What Segments Are Driving Market Leadership?

-

By Axle Type: Drive axles command a dominant 65% market share, the backbone for passenger cars, LCVs, and heavy trucks seeking robust torque and long service cycles. Lift axles are growing rapidly, prized by logistics operators for their operational flexibility and fuel-saving potential.

-

By Vehicle Type: Passenger cars reign with 61% of total market value, thanks to an installed base exceeding 259 million in the EU. The LCV segment is set to grow fastest, propelled by e-commerce and urban fleet renewals.

-

By Propulsion: Internal Combustion Engine (ICE) axles are leaders (85% share in 2024), trusted for durability—yet EV axles are scaling faster, boosted by record battery EV registrations and a rapid shift to compact, regenerative e-axles.

-

By Material: Steel remains the axle material of choice (73% share in 2024) due to its strength, cost-effectiveness, and worldwide long-term supply chains. However, lightweight composites are seeing the fastest CAGR as automakers seek to offset battery mass and unlock new vehicle efficiencies.

-

By Sales Channel: OEM supply chains dominate with 70% share, as automaker demand for quality and certified performance remains paramount. Aftermarket sales are accelerating on the back of vehicle fleet aging and the need for affordable axle solutions.

What Opportunities and Trends Will Define the Automotive Axle Decade?

Can Infrastructure Investments in Emerging Regions Fuel Market Expansion?

Ongoing infrastructure spends in Asia Pacific, the Middle East, and Africa especially in mining, heavy industry, and transport corridors—are creating huge demand for robust, high-torque axle systems for trucks, buses, and construction machinery. Major suppliers like ZF Friedrichshafen, Schaeffler, and Continental are investing in heavy-duty axle innovations tailored for extreme conditions.

Will Composites Overtake Steel as the Material of Choice?

Composites are experiencing explosive growth potential, particularly in electric and lightweight high-performance vehicles. Their superior weight savings can offset the added battery load in EVs, enhance energy efficiency, and boost range. Continued R&D and scale-up of composite axle production may well challenge the current steel hegemony in years ahead.

What Challenges Are Hindering Market Growth?

Despite the buoyant outlook, high costs for advanced alloys, electronics, and precision components limit the transition to next-gen axles—especially in price-sensitive emerging regions. Raw material sourcing uncertainties, semiconductor shortages, and production delays also pressure margins and fleet upgrade cycles. Aftermarket growth helps counter some cost pressures as fleets age and maintenance demand rises.

Automotive Axle Market Companies

- American Axle & Manufacturing Holdings, Inc.

- BASF SE

- BorgWarner Inc.

- Cummins Inc.

- Daimler AG

- Dana Incorporated

- Eaton Corporation plc

- GKN Automotive Limited

- Hyundai Transys Inc.

- Iveco Group NV

- JTEKT Corporation

- Knorr-Bremse AG

- Magna International Inc.

- MAN Truck & Bus AG

- Meritor Inc.

- Schaeffler Technologies AG & Co. KG

- Shaanxi Automobile Group Transmission Co., Ltd.

- Shaanxi Fast Auto Drive Group Co., Ltd.

- Volkswagen Group Components

- ZF Friedrichshafen AG

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6898

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026