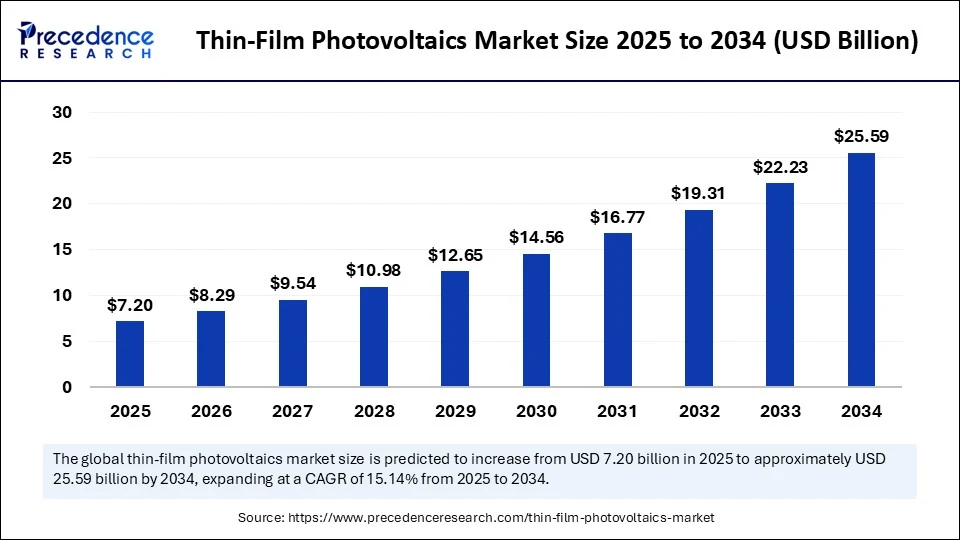

The global thin-film photovoltaics market is poised for remarkable expansion, forecasted to grow from USD 7.20 billion in 2025 to an impressive USD 25.59 billion by 2034, reflecting a strong compound annual growth rate (CAGR) of 15.14%.

This surge is fueled by escalating global investments in renewable energy, increased demand for lightweight and high-efficiency solar modules, and growing applications in utility-scale and building-integrated photovoltaics (BIPV).

Thin-Film Photovoltaics Market Key Insights

-

The market size was USD 6.25 billion in 2024 and is expected to reach USD 25.59 billion by 2034 with a CAGR of 15.14% from 2025 to 2034.

-

Asia Pacific leads the market with a dominant share of approximately 45% in 2024, valued at USD 2.81 billion, projected to grow to USD 11.64 billion by 2034.

-

Europe is the fastest-growing region due to strict building energy standards and increasing adoption of BIPV.

-

Cadmium telluride (CdTe) technology holds the largest market share at 45% attributed to its cost-effectiveness and durability.

-

Utility-scale power plants represent the largest application segment, accounting for nearly half of installations worldwide.

-

The energy & power utilities sector is the top end-user with a 55% market share, propelled by grid-connected solar farms.

-

Direct-to-project developers dominate the distribution channel with 58% market share, optimizing logistics and project customization.

AI’s Transformative Role in Thin-Film Photovoltaics

Artificial Intelligence (AI) is revolutionizing the thin-film photovoltaics landscape by enhancing operational efficiencies across the value chain. AI-driven process controllers refine deposition methods, monitor material consistency, and detect micro-level defects, ensuring minimal material wastage and consistent module performance.

Moreover, with increasing global urgency for decarbonization, AI integration supports optimized competitiveness and long-term sustainability of thin-film photovoltaics, enabling manufacturers and investors to scale production and improve energy output reliability.

What Key Factors Are Driving the Growth of the Thin-Film Photovoltaics Market?

The market growth is primarily driven by accelerating investments in renewable energy infrastructure, rapid demand for flexible and lightweight solar modules, and rising adoption in utility-scale and building-integrated applications. Technological advancements in thin-film materials such as CdTe, copper indium gallium selenide (CIGS), and perovskite offer superior weight-to-power ratios and adaptability to varied surfaces, including rooftops, building facades, and electric vehicles. Government incentives like India’s Production-Linked Incentive (PLI) and the EU’s Energy Performance of Buildings Directive 2024 significantly foster market expansion.

What Opportunities and Trends Are Shaping the Future of Thin-Film Photovoltaics?

-

How will the rise of building-integrated photovoltaics influence urban infrastructure development?

-

Can perovskite thin-film technology redefine efficiency and cost benchmarks in solar energy generation?

-

Will vehicle-integrated photovoltaics transform the electric vehicle market by reducing grid dependency?

The increasing focus on BIPV is driving thin-film adoption in facades and transparent solar glass, while perovskite segments promise rapid efficiency gains. Furthermore, the automotive sector’s push towards integrating solar into transport systems is catalyzing flexible thin-film demand.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6697

Thin-Film Photovoltaics Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 25.59 Billion |

| Market Size in 2025 | USD 7.20 Billion |

| Market Size in 2024 | USD 6.25 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 15.14% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | Europe |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Technology, Module Type, End-User Industry, Application, Distribution Channel, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Thin-Film Photovoltaics Market Regional and Segment Highlights

Asia Pacific remains the dominant region backed by large-scale solar parks in China, India, and Southeast Asia. Europe is the fastest-growing market, spearheaded by stringent energy construction codes and rising BIPV projects. Other regions such as North America and Latin America are witnessing growing investments and strategic initiatives supporting thin-film technologies.

Technology & Module Type

Cadmium telluride (CdTe) technology leads due to cost-effectiveness and robust performance, followed by rapidly growing perovskite thin-films noted for efficiency breakthroughs. In terms of modules, rigid thin-film dominates with 60% revenue share, favored in utility-scale setups, whereas flexible modules are projected to grow fastest given their adaptability and lightweight features.

End-Use and Application

The energy and power utilities sector captures the largest market share, with substantial implementation of CdTe and CIGS in grid-tied farms. Utility-scale installations remain the predominant application, while BIPV is the fastest-growing segment, driven by architectural integrations in energy-positive buildings. The automotive and transportation segments are emerging rapidly, driven by integrated solar solutions in electric vehicles and public transport.

Challenges and Cost Pressures

Despite promising growth, the thin-film photovoltaics market faces challenges such as shorter lifespan and degradation of thin-film modules compared to crystalline silicon panels, which dampens investor confidence in certain markets. High capital expenditure for manufacturing facilities also poses entry barriers for new players.

Case Study Highlight

The European Commission’s Renovation Wave Strategy (2024) targets renovation of over 35 million buildings by 2030, promoting extensive adoption of thin-film BIPV technologies in windows, façades, and rooftops, an initiative that exemplifies large-scale market integration with sustainability goals.

Leading Companies Driving Innovation

Notable market players advancing thin-film photovoltaics include First Solar (CdTe recycling initiatives), Oxford PV and National Renewable Energy Laboratory (NREL) (perovskite-silicon tandem cell efficiencies), Hanergy, and CNBM, among others specializing in semi-transparent and flexible modules.

Read Also: Distributed Energy Resources (DER) Technology Market

Take the Next Step — Download Our Thin-Film Photovoltaics Market Report

For a comprehensive analysis and tailored insights, download the full Precedence Research thin-film photovoltaics market report now or schedule a meeting with our experts to discuss strategic growth opportunities in this exciting sector.

Contact: sales@precedenceresearch.com

Explore authentic market intelligence that empowers your business decisions with data-driven, current insights in the growing thin-film photovoltaics space.