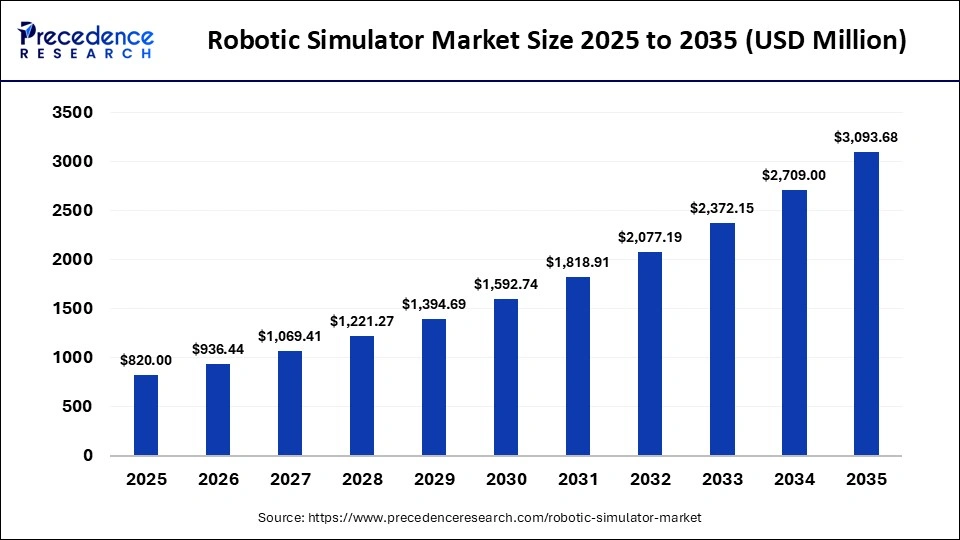

The robotic simulator market is entering a high-growth phase, driven by the convergence of robotics, artificial intelligence (AI), cloud computing, and digital twin technologies. From a valuation of USD 820 million in 2025, the market is projected to reach USD 3.09 billion by 2035, expanding at a CAGR of 14.20%.

Read Also: Data Converter Market

Deep Market Evolution: From Testing Tools to Digital Twin Ecosystems

Earlier robotic simulators were primarily used for offline programming and visualization. However, today’s platforms integrate:

- Physics-based engines

- AI-driven behavioral models

- Real-time sensor simulation

- Cloud-based collaborative environments

This shift has transformed robotic simulation into a mission-critical layer in Industry 4.0 ecosystems.

Key Evolution Phases:

- Phase 1 (Pre-2015): Basic simulation for robot path planning

- Phase 2 (2015–2020): Integration with CAD and automation systems

- Phase 3 (2020–Present): AI-enabled, cloud-integrated digital twins

- Phase 4 (Future): Fully autonomous simulation ecosystems with self-learning robots

Impact of Artificial Intelligence: The Core Growth Multiplier

Artificial intelligence is fundamentally reshaping robotic simulation capabilities.

1. Intelligent Simulation Environments

AI enables simulators to:

- Adapt to dynamic scenarios

- Learn from user behavior

- Generate predictive outcomes

2. Reinforcement Learning Integration

Robots can now be trained in simulation using reinforcement learning before deployment, significantly reducing real-world risks.

3. Synthetic Data Generation

AI-powered simulators generate massive datasets for:

- Autonomous vehicle training

- Medical robotics validation

- Industrial automation optimization

4. Real-Time Decision Intelligence

Simulators are increasingly capable of:

- Predicting failures

- Suggesting optimal actions

- Automating system adjustments

This reduces time-to-market, improves accuracy, and minimizes operational risks.

Market Drivers: Core Forces Accelerating Growth

1. Explosion of Industrial Automation

The rise of smart factories and Industry 4.0 is creating massive demand for robotic simulation tools. Manufacturers are using simulators to:

- Optimize production lines

- Reduce downtime

- Improve throughput

2. Surge in Surgical and Medical Robotics

Healthcare is becoming a major adoption hub due to:

- Need for precision surgeries

- Training without patient risk

- Simulation-based certification

3. Cost Reduction in Robotics Deployment

Physical prototyping is expensive and time-consuming. Simulation:

- Reduces hardware dependency

- Accelerates product development

- Minimizes costly errors

4. Increasing Complexity of Robotic Systems

Modern robots involve:

- Multi-axis movement

- AI-based decision-making

- Human-robot collaboration

Simulation is essential to validate such complexity.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 820.00 Million |

| Market Size in 2026 | USD 936.44 Million |

| Market Size by 2035 | USD 3,093.68 Million |

| Market Growth Rate from 2026 to 2035 | CAGR of 14.20% |

| Dominating Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Component, Deployment Mode, Application, End User, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Restraints: Challenges Hindering Adoption

1. Data Security & Privacy Risks

Particularly in healthcare and defense:

- Sensitive data exposure risks

- Regulatory compliance challenges

2. High Initial Setup Costs

Advanced simulation platforms require:

- High-performance computing infrastructure

- Skilled workforce

3. Lack of Standardization

Different simulation platforms may not be fully compatible, creating integration challenges.

Market Opportunities: High-Growth Areas

1. Digital Twin Expansion

Digital twins are becoming central to:

- Predictive maintenance

- Real-time monitoring

- Lifecycle optimization

2. Autonomous Vehicles & Drones

Simulation is critical for:

- Testing edge-case scenarios

- Validating AI decision-making

- Ensuring safety compliance

3. Robotics-as-a-Service (RaaS)

Cloud-based simulation is enabling:

- Subscription-based robotics solutions

- Remote deployment and management

4. Education & Skill Development

Universities and training institutes are increasingly adopting simulators to:

- Provide hands-on robotics training

- Reduce infrastructure costs

Segment Deep Dive

Component Analysis: Software vs Services

Software Segment (72% Share in 2025)

The dominance of software is driven by:

- Digital twin platforms

- AI-based simulation engines

- Offline programming tools

Key capabilities include:

- Motion planning

- Collision detection

- Real-time analytics

Services Segment (Fastest Growth)

Services are gaining traction due to:

- Customization needs

- Integration with enterprise systems

- Training and support requirements

This reflects a shift from product-based to solution-based models.

Deployment Mode Analysis

On-Premises (60% Share)

Preferred for:

- High-security environments

- Low-latency requirements

- Custom configurations

Widely used in:

- Defense

- Healthcare

- Large manufacturing enterprises

Cloud-Based (Fastest Growing)

Cloud adoption is accelerating due to:

- Scalability

- Cost efficiency

- Remote collaboration

Cloud simulation enables:

- Multi-user access

- Parallel simulations

- Reduced hardware dependency

Application Analysis

Industrial Robotics (45% Share)

Dominates due to:

- Automation in manufacturing

- Demand for efficiency and cost reduction

Use cases:

- Assembly line optimization

- Welding and painting simulation

- Material handling

Autonomous Vehicles & Drones (Fastest Growth)

Driven by:

- Increasing adoption of self-driving technologies

- Need for extensive safety validation

Simulators allow:

- Testing millions of driving scenarios

- Drone flight optimization

Medical Robotics

Growth driven by:

- Robotic-assisted surgeries

- Simulation-based training

Research & Education

Expanding due to:

- Integration of robotics in curricula

- Remote learning environments

End-User Analysis

Manufacturing (38% Share)

The largest adopter due to:

- Smart factory initiatives

- Automation demand

- Cost optimization

Aerospace & Defense (Fastest Growing)

Growth drivers:

- Mission-critical simulations

- Robotics in defense operations

- Space exploration

Healthcare

Key factors:

- Precision medicine

- Automation in diagnostics and labs

Automotive

Robotic simulation is essential for:

- Production line optimization

- Autonomous vehicle development

Regional Deep Dive

North America (Market Leader – 36%)

Key strengths:

- Advanced robotics ecosystem

- High R&D investments

- Early adoption of AI and simulation

The U.S. dominates due to:

- Strong manufacturing base

- Government support for robotics innovation

Asia Pacific (Fastest Growing)

Growth drivers:

- Rapid industrialization

- Government initiatives

- Expansion of manufacturing sector

China leads due to:

- Strong policy support

- Large-scale automation adoption

Europe (Second Largest – 28%)

Key factors:

- Established automation industry

- Strong regulatory framework

- Industry 4.0 initiatives

The UK and Germany are major contributors.

Competitive Landscape: Innovation-Driven Market

The market is highly competitive, with companies focusing on:

- AI integration

- Cloud-based platforms

- Strategic partnerships

Key Players:

- ABB Ltd.

- KUKA AG

- FANUC Corporation

- Yaskawa Electric Corporation

- Siemens AG

- Dassault Systèmes

- NVIDIA Corporation

- Rockwell Automation, Inc.

Recent Innovations & Strategic Developments

- Integration of simulation platforms with AI frameworks is enabling near real-world accuracy (~99%)

- Cloud-native simulation workflows are improving collaboration and scalability

- Increasing focus on physical AI and synthetic training environments

Future Outlook: The Rise of Autonomous Simulation Ecosystems

The robotic simulator market is moving toward a future where:

- Simulators will act as decision-making engines

- Robots will be trained entirely in virtual environments before deployment

- AI-driven simulations will continuously optimize real-world operations

Key Future Trends:

- Hyper-realistic physics engines

- Integration with metaverse-like environments

- Fully autonomous robotic training systems

- Expansion of Robotics-as-a-Service (RaaS)

Conclusion

The robotic simulator market is not just growing—it is redefining how robotics systems are designed, tested, and deployed. As industries continue to embrace automation, AI, and digital transformation, robotic simulators will become a foundational technology across sectors.

With strong growth across manufacturing, healthcare, autonomous systems, and defense, the market is poised to play a critical role in shaping the future of intelligent automation worldwide.