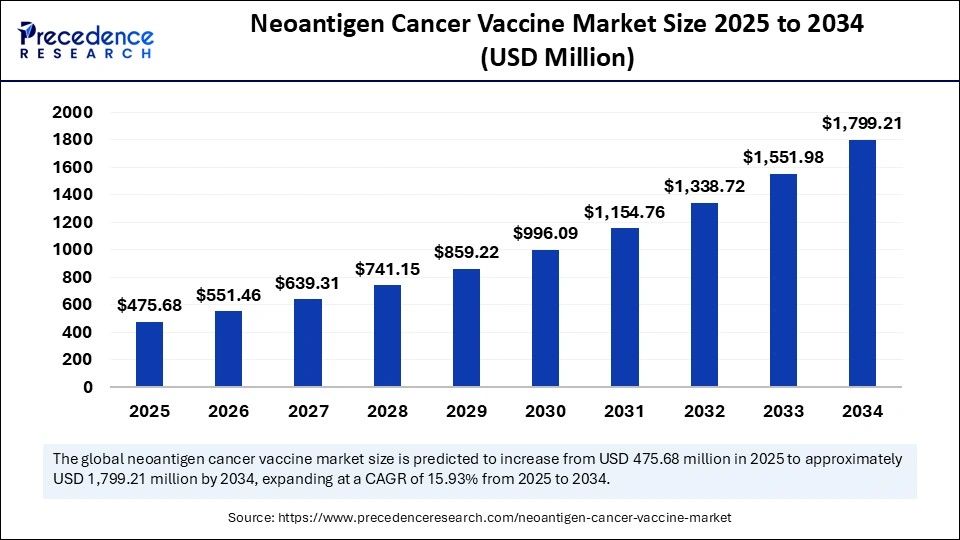

The global neoantigen cancer vaccine market was valued at USD 475.68 million in 2025 and is forecasted to escalate impressively to approximately USD 1,799.21 million by 2034, representing a compounded annual growth rate (CAGR) of 15.93% from 2025 to 2034.

This promising growth is driven by the rising global burden of cancer, increased government investments in innovative cancer therapies, and technological breakthroughs in personalized immunotherapy designed to target tumor-specific mutations.

What Makes Neoantigen Cancer Vaccines a Game-Changer in Oncology?

Neoantigen cancer vaccines represent a leap in precision oncology. They exploit unique tumor-specific mutations absent in normal cells to elicit a highly targeted immune response, offering patients therapies that are more effective and less toxic. As cancer incidence rises worldwide, the demand for such personalized immunotherapies grows, positioning the neoantigen vaccine market as a vital sector within biopharmaceutical innovation.

Neoantigen Cancer Vaccine Market Key Insights

-

The market was valued at USD 475.68 million in 2025 and is projected to reach USD 1.8 billion by 2034.

-

North America leads the market with nearly 45% of the global share, with the U.S. at the helm.

-

Asia Pacific is the fastest-growing region, driven by demographic shifts and rising cancer cases.

-

The personalized neoantigen vaccines segment holds around 70% revenue share in 2024.

-

mRNA-based vaccines dominate the technology platform segment with 50% market share.

-

Melanoma is the leading cancer type targeted, with 40% market share.

-

Top players include Moderna Inc., BioNTech SE, Merck & Co., F. Hoffmann-La Roche Ltd., and Gritstone bio, Inc.

Market Scope

| Metric | USD Million |

|---|---|

| Market Size in 2025 | 475.68 |

| Market Size in 2026 | 551.46 |

| Market Size by 2034 | 1,799.21 |

| CAGR (2025-2034) | 15.93% |

| U.S. Market Size (2025) | 171.24 |

| U.S. Market Size (2034) | 659.21 |

AI is revolutionizing how neoantigen cancer vaccines are developed, enabling more precise, faster, and personalized therapies. By analyzing complex genomic, transcriptomic, and proteomic data from patient tumors, AI models identify mutated peptides most likely to stimulate a strong immune response. These include assessments of MHC binding affinity, peptide stability, and T-cell receptor interaction, dramatically refining the vaccine design process.

Furthermore, AI accelerates the vaccine pipeline from neoantigen candidate identification to optimized delivery methods, ensuring personalized vaccines are developed rapidly and with enhanced specificity. This integration of AI technology is critical to meeting the growing demand for effective, tailored cancer immunotherapies in clinical settings.

Key Market Growth Factors

-

Increasing cancer prevalence globally, driving demand for advanced therapies.

-

Government and private sector investments in cancer vaccine R&D.

-

Technological innovations such as next-generation sequencing and mRNA platforms.

-

Rising adoption of personalized medicine approaches targeting tumor heterogeneity.

-

Expansion of combination therapies using neoantigen vaccines with immune checkpoint inhibitors.

What Are the Current Opportunities and Emerging Trends in the Market?

How are combination therapies shaping the neoantigen cancer vaccine landscape?

Combining neoantigen vaccines with immune checkpoint inhibitors enhances antitumor immune responses, expanding efficacy for patients who do not respond to monotherapies. This synergistic approach is opening new frontiers for personalized cancer treatment.

Why is the Asia Pacific region poised for rapid growth?

The region faces demographic shifts with an aging population, responsible for nearly 60% of global cancer cases. Increasing healthcare investments and government initiatives such as China’s “Healthy China 2030” are propelling market expansion.

What makes mRNA-based vaccines dominant in technology platforms?

Their rapid design, flexibility, scalable manufacturing, and cost-effectiveness make mRNA vaccines ideal for personalized, tumor-specific immunotherapies, accounting for half of the market share.

Segmental Insights

Product Type Insights: Personalized Vaccines Lead

In 2024, personalized neoantigen vaccines held about 70% of the market share. Their ability to target patient-specific tumor mutations while sparing healthy cells drives their dominance. By stimulating neoantigen-driven T-cell responses, these vaccines provide a diversified immune attack with fewer off-target effects.

Off-the-shelf neoantigen vaccines are expected to grow the fastest due to their cost-effectiveness, scalability, and faster production. Advances in mRNA platforms and next-generation sequencing enable broad-spectrum vaccines with high therapeutic potential.

Neoantigen Source Insights: Tumor Mutations Dominate

The tumor mutations segment led the market in 2024 with nearly 65% share. Its uniqueness allows highly personalized and targeted therapies with fewer side effects. Growth is supported by genomics and bioinformatics advancements, improving therapeutic precision.

The tumor-associated antigens segment is expected to grow significantly, driven by their role in early cancer detection and as a foundation for highly specific immunotherapies.

Administration Route Insights

The intravenous (IV) route dominated with approximately 60% share in 2024. IV administration ensures rapid and precise vaccine distribution, making it suitable for complex formulations like dendritic cell and nucleic acid-based therapies.

Intramuscular (IM) administration is expected to grow fastest, due to its ability to elicit strong immune responses and compatibility with mRNA-based platforms. Its practicality, safety, and minimally invasive nature boost adoption.

Technology Platform Insights

mRNA-based vaccines held around 50% market share in 2024, driven by rapid design, scalable manufacturing, and flexibility in targeting specific tumor neoantigens. They offer cost-effectiveness, tolerability, and strong immune responses.

Peptide-based vaccines are projected to grow at the highest CAGR, offering high precision, established manufacturing, customization potential, and lower toxicity compared to conventional therapies.

Application Insights

Melanoma accounted for nearly 40% of the market in 2024, thanks to its high tumor mutational burden (TMB), which generates numerous targetable antigens. Clinical trials demonstrate promising efficacy, making melanoma a preferred model for neoantigen vaccine development.

Non-small cell lung cancer (NSCLC) is expected to grow the fastest, driven by high incidence and mortality, creating strong demand for targeted and effective therapies.

End-User Insights

Biopharmaceutical companies held nearly 55% of the market in 2024, backed by strong R&D investments, collaborations with academic institutions, and expertise in clinical trials and manufacturing.

Research institutions are expected to grow fastest due to increased funding for personalized cancer research and adoption of technologies like AI to accelerate discovery and experimentation.

Regional Insights

North America captured nearly 45% of the market in 2024, supported by robust R&D funding, advanced infrastructure, and expertise in sequencing and bioinformatics for precise neoantigen identification. A mature healthcare system ensures strong market receptivity.

The U.S. leads the region with a hub of pharmaceutical giants and biotech startups leveraging mRNA technology, advanced genomics, and collaborations. FDA support for innovative cancer therapies accelerates approvals and market entry.

Asia Pacific Market Growth

Asia Pacific is expected to grow at the fastest rate due to an aging population, high cancer prevalence, and increased healthcare investments. National initiatives and local biotech collaborations further drive market expansion.

China is a key market leader, with strong government initiatives like “Healthy China 2030” and a supportive regulatory environment (NMPA), encouraging innovation and faster adoption of neoantigen cancer vaccines.

Latest Industry Breakthroughs and Company Contributions

Leading companies advancing the market include:

-

Moderna Inc: Pioneer in mRNA neoantigen vaccine platforms with robust clinical pipelines.

-

BioNTech SE: Innovator in personalized vaccine technology with extensive partnerships.

-

Merck & Co., Inc.: Key collaborator in neoantigen vaccine R&D and oncology portfolio expansion.

-

F. Hoffmann-La Roche Ltd.: Significant investor in cancer immunotherapies and clinical ventures.

-

Gritstone bio, Inc.: Developer of EDGE platform for personalized vaccines.

Other noteworthy players include OSE Immunotherapeutics, Advaxis, Agenus, Vaccibody, and Novogene, adding technological depth and service capacity across the value chain.

Challenges and Cost Pressures

Tumor heterogeneity presents a major challenge, as the genetic uniqueness of cancer cells in each patient complicates vaccine effectiveness. Manufacturing scalability, regulatory complexities, and high development costs also pose barriers to rapid market expansion.

Segments Covered in the Report

By Product Type

- Personalized Neoantigen Vaccines

- Off-the-Shelf Neoantigen Vaccines

By Neoantigen Source

- Tumour Mutations

- Tumour-Associated Antigens

By Administration Route

- Intravenous

- Intramuscular

- Transdermal

- Others

By Technology Platform

- mRNA-Based Vaccines

- Peptide-Based Vaccines

- Viral Vector-Based Vaccines

- Others

By Application

- Melanoma

- Non-Small Cell Lung Cancer (NSCLC)

- Pancreatic Cancer

- Others

By End-User

- Biopharmaceutical Companies

- Research Institutions

- Hospitals and Clinics

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Read Also: Checkpoint Inhibitor Biologics CDMO Market

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com | +1 804 441 9344