Powering the Battery Revolution: Asia Pacific Leads as Lithium Sulfides Market to Expand at 35.54% CAGR

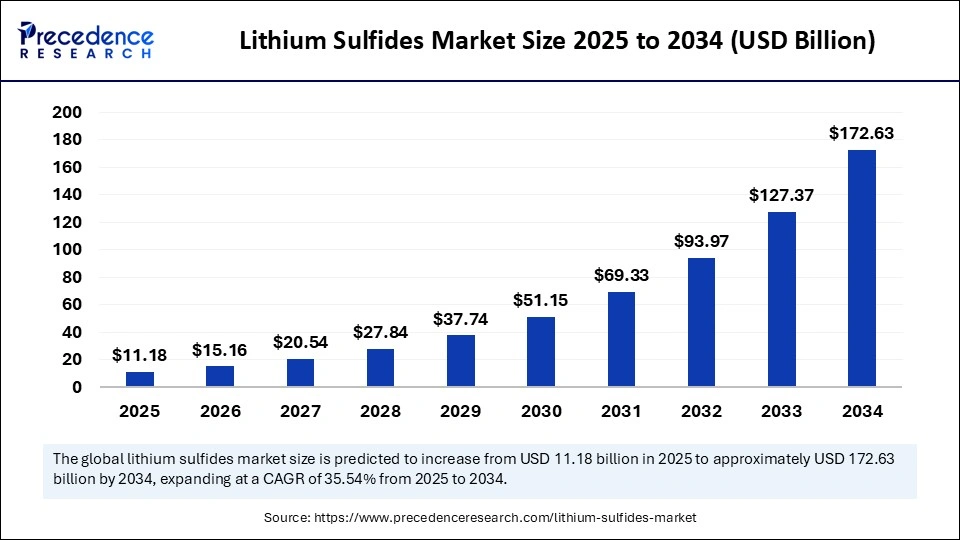

Driven by surging electric vehicle adoption, booming portable electronics sectors, and an ever-increasing demand for sustainable energy storage solutions. According to Precedence Research, the global lithium sulfides market is poised for remarkable growth. Valued at USD 8.25 billion in 2024, the market is on track to reach an astonishing USD 172.63 billion by 2034, boasting a robust CAGR of 35.54% from 2025 to 2034.

Asia Pacific maintains its dominance, while North America emerges as the fastest-growing regional market, riding the wave of technological innovation and green energy initiatives.

Lithium Sulfides Market Key Highlights

-

The global lithium sulfides market grew from USD 8.25 billion in 2024 to USD 11.18 billion in 2025, and is forecasted to reach USD 172.63 billion by 2034.

-

Asia Pacific commands the largest market share (40% in 2024), led by China and India as top contributors.

-

North America is anticipated to post the fastest growth rate through to 2034.

-

The powder form segment dominated in 2024 for its role in advanced battery and electronics components.

-

The automotive (EV battery) sector leads among end-users, fueled by supportive policies and the shift to electric mobility.

-

Direct sales to battery OEMs remain the principal distribution channel, ensuring co-development opportunities and security of supply.

-

Top industry players: (Include up-to-date list as available; see company section below.)

Lithium Sulfides Market Revenue Table

| Year | Market Size (USD Billion) | CAGR (%) |

|---|---|---|

| 2024 | 8.25 | — |

| 2025 | 11.18 | 35.54 (2025-2034) |

| 2034 | 172.63 | — |

Artificial Intelligence (AI) is rapidly becoming a game-changer for lithium sulfides and the broader solid-state battery industry. AI-infused analytics now optimize material selection, manufacturing processes, and battery design, resulting in significant gains in operational efficiency and waste reduction. From advanced material screening to predictive maintenance within lithium-sulfur battery systems, AI’s influence is fast-tracking performance improvements, longevity, and charging optimization.

Machine learning models drive breakthroughs in battery management, accurately forecasting performance dips and extending system lifespan. As manufacturers race to deploy next-generation batteries in EVs and grid storage, AI-driven innovation delivers safer, higher-density, and more reliable energy solutions.

Key Growth Factors Steering the Lithium Sulfides Market

Multiple market forces power the lithium sulfides boom:

-

Surging adoption of EVs and portable electronics pushes demand for next-gen batteries.

-

Government emissions targets and regulatory policies propel clean energy solutions.

-

Advancements in solid-state, Li-S battery chemistries enable higher energy density and improve safety.

-

Expanding applications beyond energy storage—into catalysts, electronics, and chemical intermediates—widen lithium sulfides’ appeal.

What Opportunities and Trends Can Stakeholders Leverage?

How Is Grid-Scale Energy Storage Reshaping the Market?

The global shift toward renewable energy brings unprecedented opportunities. Utilities increasingly seek lithium-sulfur batteries for grid-scale and residential applications due to high energy density and affordability. These batteries not only support climate goals but also address the intermittency of renewables, ensuring stable, cost-effective energy supply for both utilities and households.

Which Segments Set the Pace for Innovation?

Powdered lithium sulfides dominate for their role in batteries and electronics, while crystalline forms are expected to see rapid uptake due to their suitability as high-performance battery cathodes. In applications, the automotive sector (EV batteries) leads in revenue, while energy storage systems for grid and residential use are projected to grow swiftly.

How Crucial Are Solid-State Electrolytes in the Future of Lithium Batteries?

Solid-state battery electrolytes—largely sulfide-based—usher in a new era of energy storage by enabling all-solid lithium metal batteries. Superior ionic conductivity, safety, and longevity make them central to sustained battery innovation and the adoption of all-solid-state battery systems across industries.

Regional and Segmental Analysis: Shifting Global Dynamics

Why Does Asia Pacific Dominate the Lithium Sulfides Market?

Asia Pacific, home to 40% of the market in 2024, enjoys not only raw material abundance but also leading-edge manufacturing for EVs and electronics. China stands out as the region’s powerhouse, with large-scale production capacity for batteries and end-use devices. The region’s momentum is boosted by R&D investments, government incentives (tax breaks and subsidies), and aggressive emission reduction targets.

What Gives North America Its Fastest-Growing Status?

Rapid technological advancement, a robust base of research institutions, and green policy measures make North America the fastest-growing region. Strong demand across consumer electronics, automotive electrification, and grid innovation is amplifying market development.

Segment Highlights

Form: Powder (2024 leader) and crystalline (fastest-growing)

Application: Advanced batteries (solid-state and Li-S), specialty cathode/anode precursors, energy storage

End-Use Industry: Automotive (EVs), grid storage, portable electronics, aerospace, and specialty chemicals

Distribution Channel: Direct sales to OEMs (leader), specialty chemical distributors (quickest growth)

Lithium Sulfides Market Companies

- Nippon Chemical Industrial Co., Ltd.

- Mitsui Mining & Smelting Co., Ltd.

- NEI Corporation

- Solid Power, Inc.

- QuantumScape Corporation

- NGK Insulators Ltd.

- Samsung SDI Co., Ltd.

- Hitachi Chemical (Showa Denko Materials)

- Sumitomo Chemical Co., Ltd.

- LG Energy Solution

- CATL (Contemporary Amperex Technology)

- TDK Corporation (including Amperex Technology)

- Umicore

- Toray Industries, Inc.

- BASF SE (Battery Materials Division)

- Targray Technology International

- Stella Chemifa Corporation

- Ohara Inc.

- Ilika plc

- Murata Manufacturing Co., Ltd.

Addressing Market Challenges and Cost Pressures

Despite an optimistic outlook, key challenges persist:

-

Technical headwinds, notably around battery cycling stability and lifespan, may slow adoption.

-

High up-front investment requirements for manufacturing scale-up constrain new entrants and early-stage producers.

-

Intense competition and fluctuating raw material prices pose ongoing cost pressures, demanding efficiency and collaboration across the value chain.

Sample Case Study: Asia Pacific’s EV Battery Surge

In 2024, a leading EV battery OEM in China adopted lithium-sulfur batteries sourced locally, reducing production costs by 18% and increasing battery range by over 30%. These results highlight not only the regional advantage but also the technology’s practical impact on both performance and cost-effectiveness in the booming EV market.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6839

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344