Integrated Delivery Network Market Key Points

-

North America held the biggest revenue share of 40% in 2024.

-

Asia Pacific is expected to expand at the fastest CAGR of 12.32% between 2025 and 2034.

-

By service, the acute care segment contributed the largest revenue share in 2024.

-

By service, the long-term health segment is expected to grow at a significant CAGR during the forecast period.

-

By integration model, the vertical integration segment captured the largest revenue share in 2024.

-

By integration model, the horizontal integration segment is expected to grow at the fastest CAGR from 2025 to 2034.

-

By facility, the acute facilities segment dominated the market in 2024.

-

By facility, the outpatient facilities segment is expected to expand at the highest CAGR from 2025 to 2034.

What is the Role of AI in the Integrated Delivery Network (IDN) Market?

1. Enhancing Operational Efficiency and Care Coordination

Artificial Intelligence (AI) is revolutionizing Integrated Delivery Networks (IDNs) by streamlining workflows, improving care coordination, and optimizing resource utilization. AI algorithms can analyze large volumes of patient data across different care settings to identify gaps, reduce redundancies, and suggest evidence-based treatment plans. This not only minimizes unnecessary procedures and hospital readmissions but also ensures continuity of care—crucial in an integrated care model. Predictive analytics also helps IDNs anticipate patient needs, enabling proactive interventions and better allocation of healthcare resources.

2. Driving Personalized Care and Population Health Management

AI plays a significant role in population health by identifying high-risk patient groups and tailoring interventions accordingly. In IDNs, which aim to deliver holistic and value-based care, AI supports chronic disease management by monitoring patient data in real-time, alerting clinicians to anomalies, and suggesting personalized care plans. Furthermore, AI tools such as natural language processing (NLP) extract insights from unstructured data like clinical notes and patient feedback, enhancing clinical decision-making and patient engagement strategies across the network.

Integrated Delivery Network Market Growth Factors

The growth of the Integrated Delivery Network (IDN) market is primarily driven by the rising need for coordinated, value-based healthcare delivery systems. Healthcare providers are increasingly seeking to streamline operations, reduce redundancies, and improve patient outcomes through integrated care models. IDNs offer a centralized structure that connects hospitals, physician groups, labs, and other care facilities under a single administrative and financial system. This integration enhances care coordination, reduces medical errors, and promotes cost-efficiency—an appealing solution for both private and public healthcare systems under pressure to deliver quality care at lower costs.

Additionally, the increasing adoption of health IT solutions, such as electronic health records (EHRs), telehealth platforms, and population health management tools, significantly contributes to the market’s expansion. These technologies enable seamless data sharing and analytics across the network, facilitating proactive and personalized care. Furthermore, the shift towards alternative payment models, such as bundled payments and accountable care organizations (ACOs), is encouraging healthcare systems to adopt IDN structures to meet performance metrics and financial incentives. Aging populations, the growing burden of chronic diseases, and supportive regulatory frameworks in regions like North America and Europe further bolster the market’s upward trajectory.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6160

Market Scope

| Report Coverage | Details |

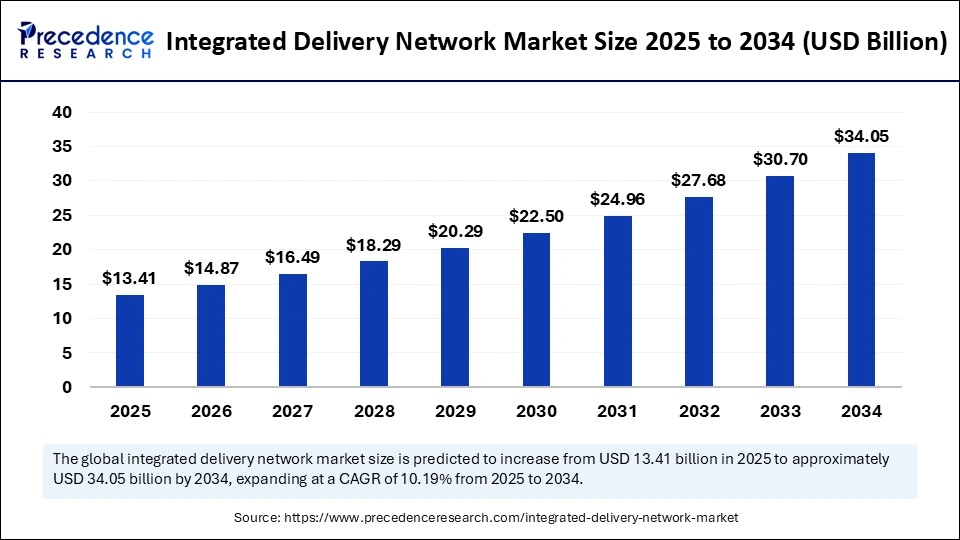

| Market Size by 2034 | USD 34.05 Billion |

| Market Size in 2025 | USD 13.41 Billion |

| Market Size in 2024 | USD 12.09 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 10.91% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Service, Integration Model, Facility, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Dynamics

Market Drivers: Emphasis on Cost-Efficient, Value-Based Care

The growing shift toward value-based healthcare is a major driver of the Integrated Delivery Network market. Healthcare systems worldwide are under pressure to improve patient outcomes while controlling costs. IDNs offer a comprehensive solution by integrating hospitals, physicians, and other healthcare services into a unified delivery system, which improves coordination and reduces redundancies.

This model enhances the ability to manage patient care more efficiently across the continuum, leading to cost savings and improved health outcomes. Additionally, increasing demand for accountable care organizations (ACOs), the rising burden of chronic diseases, and supportive government initiatives further fuel the adoption of IDNs. The growing use of electronic health records (EHRs) and telemedicine has also played a vital role in strengthening the IDN infrastructure by facilitating data sharing and remote patient management.

Opportunities: Integration of AI and Data Analytics

The integration of advanced technologies such as artificial intelligence (AI), machine learning, and big data analytics offers immense opportunities in the IDN market. AI can help analyze massive volumes of patient data to identify health patterns, predict disease outbreaks, and personalize treatment plans, thereby significantly improving the efficiency of care delivery. Predictive analytics tools are increasingly used within IDNs to enhance resource allocation and reduce hospital readmission rates.

Furthermore, as the global healthcare industry continues to digitalize, IDNs are well-positioned to adopt innovative patient engagement platforms, population health management tools, and interoperability solutions. These advancements can enhance care coordination, reduce operational costs, and expand IDNs’ capabilities in delivering high-quality and patient-centric care across regions.

Challenges: Operational Complexity and Interoperability Issues

Despite the advantages, the implementation and expansion of IDNs face several operational and technological challenges. One major hurdle is the complexity of integrating diverse healthcare entities with varying operational standards, workflows, and IT systems. Achieving seamless interoperability between disparate electronic health record systems remains a significant challenge, often leading to data silos and inefficiencies in care coordination.

Additionally, aligning the interests of different stakeholders—such as hospitals, primary care providers, and specialists—under a single governance structure can be difficult. Regulatory compliance and data security also pose substantial barriers, especially as IDNs deal with sensitive patient information and must comply with stringent healthcare laws such as HIPAA. Resistance to change among staff and inadequate training on new technologies can further delay the successful implementation of IDNs.

Regional Outlook: North America Leads, Asia-Pacific Emerges

Geographically, North America currently dominates the Integrated Delivery Network market, driven by a mature healthcare system, widespread adoption of EHRs, and strong regulatory support for coordinated care models. The U.S., in particular, has a high concentration of IDNs due to the presence of large healthcare conglomerates and favorable reimbursement frameworks. Europe follows, with growing efforts to improve cross-border healthcare interoperability and rising government investment in integrated care systems.

However, the most rapid growth is projected in the Asia-Pacific region, owing to the increasing burden of chronic diseases, healthcare infrastructure development, and digital health adoption. Countries such as China, India, and Japan are witnessing heightened investments in health IT and care coordination platforms, which are expected to accelerate the formation of IDNs. Meanwhile, Latin America and the Middle East & Africa are gradually adopting integrated care models, but market growth is somewhat restrained by limited infrastructure and regulatory challenges.

Integrated Delivery Network Market Companies

- Kaiser Permanente

- Mayo Clinic

- Cleveland Clinic

- Intermountain Healthcare

- Geisinger Health System

- UPMC (University of Pittsburgh Medical Center)

- Ascension Health

- Providence St. Joseph Health

- Trinity Health

- Sutter Health

- Baylor Scott & White Health

- Advocate Aurora Health

- Banner Health

- Dignity Health

- Henry Ford Health System

- Northwell Health

- Partners HealthCare

- Sentara Healthcare

- Spectrum Health

- Mercy

Segments Covered in the Report

By Service

- Acute Care

- Primary Care

- Long-term Health

- Specialty Clinics

- Others

By Integration Model

- Vertical

- Horizontal

By Facility

- Acute Facilities

- Outpatient Facilities

By Region

- North America

- Latin America

- Asia Pacific

- Europe

- MEA

Also Read: Silicon Anode Battery Market

Source: https://www.precedenceresearch.com/integrated-delivery-network-market

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026