eHealth 2.0 Market Key Highlights

-

North America dominated the eHealth 2.0 market in 2024.

-

Europe is expected to grow at a significant CAGR during the forecast period.

-

By type, the telemedicine segment held the largest market share in 2024.

-

The electronic health records segment is projected to expand at a significant CAGR in the upcoming period.

-

By service, the monitoring segment contributed the major market share in 2024.

-

The diagnosis segment is expected to grow at a notable CAGR in the coming years.

-

By end-user, the healthcare providers segment captured the biggest market share in 2024.

-

The insurers segment is anticipated to grow at a notable CAGR during the forecast period.

eHealth 2.0 Overview

eHealth 2.0 refers to the next generation of digital healthcare services that integrate Web 2.0 technologies—such as social networking, cloud computing, mobile apps, and user-generated content—into healthcare delivery. Unlike traditional eHealth systems that focused on digitizing medical records and administrative processes, eHealth 2.0 emphasizes collaboration, real-time communication, and patient empowerment. It allows patients, doctors, and healthcare providers to interact more directly through digital platforms, improving access to care and health literacy.

Key Features and Impact

eHealth 2.0 includes tools like telemedicine, wearable health monitors, mobile health apps, and online patient communities. These innovations support remote consultations, continuous health monitoring, and data sharing, leading to more personalized and proactive healthcare. The platform fosters patient engagement, improves chronic disease management, and enhances decision-making through real-time data analytics. With growing internet connectivity and smartphone adoption, eHealth 2.0 is transforming healthcare into a more accessible, efficient, and patient-centered ecosystem.

How is AI Powering the eHealth 2.0 Revolution?

Artificial Intelligence is a key driver of the eHealth 2.0 market, enabling more personalized, efficient, and proactive healthcare delivery. AI-powered platforms integrate electronic health records (EHRs), Internet of Medical Things (IoMT) devices, edge computing, and cloud services to monitor patient data in real time. This allows for early detection of health issues, prioritization of high-risk patients, and improved chronic disease management. By supporting remote monitoring and predictive analytics, AI reduces the burden on healthcare systems while enhancing patient outcomes and care efficiency.

Additionally, AI in eHealth 2.0 is focused on transparency, security, and reliability. Explainable AI models help healthcare professionals and patients understand the reasoning behind clinical recommendations, fostering trust in automated decisions. Combined with secure data management systems like blockchain and edge-cloud infrastructure, AI ensures the confidentiality and integrity of sensitive health data. These advancements elevate eHealth platforms from basic digital tools to intelligent, secure, and responsive healthcare ecosystems.

Growth Drivers of the eHealth 2.0 Market

Expansion of Telemedicine, mHealth, and Patient-Centric Care

The surge in telemedicine and mobile health (mHealth) adoption, accelerated by the COVID-19 pandemic, is a primary catalyst for eHealth 2.0 growth. Patients and providers increasingly prefer remote consultations, real-time monitoring, and digital health records for chronic disease management and preventive care. Widespread smartphone penetration, wearable technology integration, and immersive patient engagement tools support 24/7 healthcare access, improving outcomes and operational efficiency.

Technological and Regulatory Tailwinds

Advancements in AI, machine learning, big data analytics, and IoT are revolutionizing diagnostic accuracy, predictive healthcare, and administrative automation in eHealth. These technologies empower clinicians to derive actionable insights from large data volumes, enhancing personalized medicine and reducing clinical errors. Strong government initiatives, support for digital record systems, and incentive programs further drive market expansion across regions like North America and Asia-Pacific.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview@ https://www.precedenceresearch.com/sample/6170

Market Scope

| Report Coverage | Details |

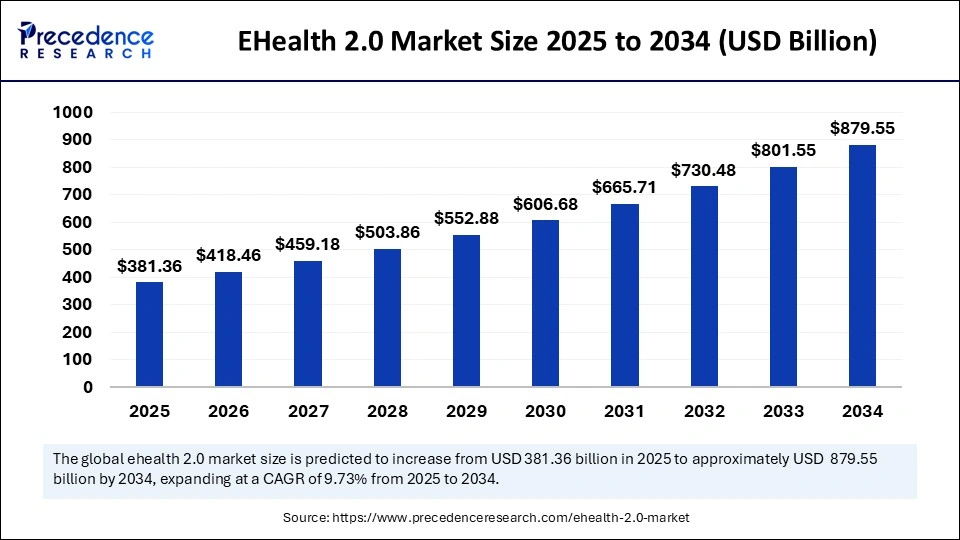

| Market Size by 2034 | USD 879.55 Billion |

| Market Size in 2025 | USD 381.36 Billion |

| Market Size in 2024 | USD 347.54 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 9.73% |

| Dominating Region | North America |

| Fastest Growing Region | Europe |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Type, Service, End User, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Dynamics

Market Drivers

The eHealth 2.0 market is being propelled by the increasing demand for patient-centric digital health solutions that leverage advanced technologies such as AI, big data, IoT, and cloud computing. As healthcare systems shift from volume-based to value-based care, the need for integrated platforms that enhance clinical decision-making, improve patient engagement, and reduce healthcare costs is more pronounced than ever. The proliferation of smartphones and wearable devices, coupled with rising internet penetration, has made real-time health monitoring and teleconsultation more accessible and reliable.

Moreover, the COVID-19 pandemic significantly accelerated digital transformation in healthcare, making eHealth platforms mainstream across both developed and developing economies. Government initiatives supporting digital health ecosystems, including electronic health records (EHR), telemedicine regulations, and national digital health missions, are also key drivers of market growth.

Opportunities

The eHealth 2.0 market presents vast opportunities in expanding preventive care, remote patient monitoring, and personalized medicine. The integration of AI and machine learning into eHealth platforms allows for predictive analytics, enabling early diagnosis and proactive intervention for chronic diseases such as diabetes, cardiovascular disorders, and mental health conditions. Furthermore, the rise of blockchain in healthcare offers potential for secure patient data exchange and tamper-proof electronic medical records. There is also a growing market for mental health apps, virtual wellness platforms, and AI-driven health assistants.

In emerging markets, the unmet demand for quality healthcare services and the shortage of healthcare professionals make mobile health (mHealth) and virtual care critical, presenting significant untapped potential. Partnerships between technology firms and healthcare providers are opening new avenues for hybrid care models that blend in-person and digital services.

Challenges

Despite the optimistic outlook, the eHealth 2.0 market faces several challenges. Data privacy and security remain major concerns, as the increasing volume of digital health data is a prime target for cyberattacks and breaches. Interoperability between different health IT systems continues to be a hurdle, hampering the seamless exchange of patient information across platforms and providers. Regulatory fragmentation across countries and even within regions makes it difficult for eHealth solutions to scale globally.

Additionally, digital literacy and access inequalities limit adoption, especially among older adults and rural populations. Resistance to change from traditional healthcare stakeholders and issues related to the reimbursement of telehealth services can also slow down broader market penetration. Ensuring evidence-based validation of digital health tools remains essential for clinical credibility and acceptance.

Regional Outlook

North America leads the eHealth 2.0 market, driven by advanced healthcare infrastructure, high adoption of digital technologies, and supportive regulatory frameworks, including HIPAA compliance and Medicare support for telehealth. The U.S. continues to be the primary contributor due to its dynamic health tech startup ecosystem and growing patient demand for convenient care models. Europe is another significant market, benefiting from initiatives like the EU Digital Health Strategy and strong emphasis on integrated care and cross-border health data sharing. Germany, the UK, and the Nordics are at the forefront of innovation and adoption.

Asia-Pacific is witnessing rapid growth, propelled by large population bases, rising healthcare expenditures, and strong governmental support for digital health. China and India, in particular, are advancing fast with mobile health adoption, AI-based diagnostics, and cloud-based hospital platforms. Latin America and the Middle East & Africa are gradually embracing eHealth technologies, with progress being driven by public-private partnerships and efforts to overcome healthcare delivery gaps, though limited infrastructure and digital access still pose significant challenges in these regions.

eHealth 2.0 Market Companies

- Athenahealth Inc.

- iCliniq

- Medtronic

- Epocrates

- Medisafe

- Teladoc Health, Inc.

- LiftLabs

- CompuMed Inc.

- GE Healthcare

- Telecare Corporation

- Optum Health

- Siemens Healthineers

- Veradigm LLC

- eClinicalWorks

Segments Covered in the Report

By Type

- Telemedicine

- Electronic Health Records (EHRS)

- E-Prescription

- Remote Patient Monitoring

- mHealth

- Health Information Exchange (HIE)

- Others

By Service

- Monitoring

- Diagnostic

- Treatment

By End-User

- Healthcare Providers

- Insurers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa (MEA)

Also Read:Investigational New Drug CDMO Market

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com|+1 804 441 9344