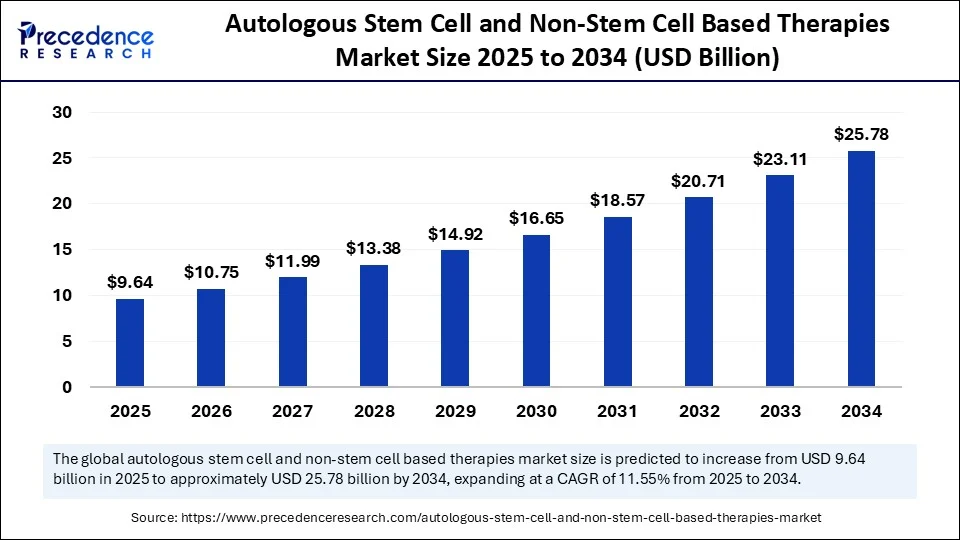

The autologous stem cell and non-stem cell based therapies market is projected to expand from approximately USD 9.64 billion in 2025 to around USD 25.78 billion by 2034. This growth corresponds to a strong CAGR of 11.55%, showcasing the sector’s rapid evolution driven by technological advancements and rising demand for personalized medicine.

The regenerative medicine landscape is evolving swiftly, propelled by increasing chronic and degenerative disease prevalence worldwide. Patients’ demand for effective, personalized cell therapies that minimize immune rejection has pushed autologous therapies to the forefront. Innovations in clinical applications for cardiology, neurology, orthopedics, and oncology, alongside growing regulatory approvals, have been key forces driving a CAGR of 11.55% during the forecast period.

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Key Insights

-

The market was valued at USD 8.64 billion in 2024 and is expected to more than triple by 2034 to USD 25.78 billion.

-

North America is the largest regional market, primarily driven by the U.S.’s advanced healthcare infrastructure.

-

Asia Pacific holds the position as the fastest-growing region due to government backing and rising medical tourism.

-

The U.S. market alone is forecasted to jump from USD 2.42 billion in 2024 to USD 7.36 billion by 2034.

-

Top players leading innovation include Bristol-Myers Squibb, Gilead Sciences, Novartis, Johnson & Johnson, and Caladrius Biosciences.

What Are the Key Market Drivers Accelerating This Growth?

The escalating burden of chronic ailments such as cancer, cardiovascular disorders, diabetes, and neurodegenerative diseases has amplified the need for innovative therapeutic interventions. Autologous therapies, which utilize a patient’s own cells, reduce immune rejection risk and ethical concerns, making them highly preferred. Enhanced R&D, novel clinical applications in orthopedics, cardiology, neurology, and expanded regulatory approvals are further catalyzing market momentum.

How is AI Shaping the Future of Autologous Therapies?

Artificial Intelligence (AI) is playing a transformative role by driving precision medicine in autologous and non-autologous cell therapies. AI facilitates personalized treatment regimens through advanced cell characterization, optimizing cell differentiation processes and enhancing diagnostic accuracy. Its ability to analyze large clinical datasets expedites the identification of optimal cell products tailored for individual patient needs.

Moreover, AI-driven advanced microscopy and imaging techniques enable precise, non-invasive live cell analysis for early diagnosis and continuous treatment monitoring. This integration accelerates therapy development for complex diseases like diabetes and liver ailments, enhancing overall patient outcomes in regenerative medicine.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6678

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 25.78 Billion |

| Market Size in 2025 | USD 9.64 Billion |

| Market Size in 2024 | USD 8.64 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 11.55% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Therapy Type, End User, Application, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Regional and Segment Analyses

North America’s Market Leadership

North America dominated the global autologous stem cell and non-stem cell based therapies market in 2024, primarily due to its well-developed healthcare infrastructure, advanced clinical research and development ecosystem, and a pro-innovation regulatory environment. The presence of strong healthcare systems ensures efficient delivery and growth of complex cell therapies. Additionally, the rising prevalence of chronic diseases such as cardiovascular disorders, cancer, and neurodegenerative diseases drives demand for innovative regenerative treatments.

The U.S., as the core country in this region, leads through extensive clinical trials, expedited regulatory pathways like the regenerative medicine advanced therapy designation, and increased FDA approvals, particularly for CAR T-cell therapies. For example, in June 2025, the FDA updated labels for CAR T-cell therapies Breyanzi (liso-cel) and Abecma (ide-cel), reducing patient monitoring requirements and eliminating REMS programs to expand accessibility to eligible blood cancer patients. This reflects growing confidence in the safety and efficacy of these therapies and supports increased uptake in the market.

Asia Pacific’s Rapid Growth

Asia Pacific is forecasted as the fastest-growing region due to its large patient population, increasing prevalence of chronic diseases, and supportive government policies. Countries such as Japan and South Korea have implemented regulatory frameworks like Japan’s Regenerative Medicine Promotion Act, which streamline product approvals. Emerging economies including India and China benefit from growing medical tourism and investments in GMP-certified facilities for cell therapy manufacturing. These factors combine to foster significant market expansion in the region.

Segment-wise Market Breakdown

-

Therapy Type: The autologous stem cell-based therapies segment holds the largest market share due to minimized risks of immune rejection and ethical considerations. These therapies are widely preferred for their safety and regenerative potential.

-

Fastest Growing Therapy: Autologous non-stem cell based therapies are growing the fastest, driven by CAR T-cell therapies and platelet-rich plasma (PRP) treatments. Their expanding applications beyond oncology, into autoimmune diseases and solid tumors, enhance their growth trajectory.

-

Application: Oncology leads with the highest market contribution, propelled by the rising incidence of cancers and the availability of cell-based immunotherapies like CAR T-cell therapy. Neurology is anticipated to be the fastest growing application segment because of increasing neurodegenerative disorders, such as Alzheimer’s and Parkinson’s diseases, benefiting from regenerative approaches.

-

End User: Hospitals and clinics dominate due to established infrastructure and capacity to manage complex cell-based therapies. However, specialized cell therapy centers are rapidly rising fueled by increasing chronic disease cases and regulatory green lights for advanced therapies.

What Are the Latest Breakthroughs and Who Are the Key Players?

Recent Breakthroughs

Significant advancement includes the U.S. FDA’s June 2025 label updates for CAR T-cell therapies Breyanzi (Bristol-Myers Squibb) and Abecma (Gilead Sciences). These changes reduce post-treatment monitoring burdens and eliminate Risk Evaluation and Mitigation Strategies (REMS), allowing broader patient access and addressing the previous underutilization where only 20% of eligible patients could benefit from these therapies. This regulatory shift marks a milestone in making cell therapy more accessible and scalable in treating hematologic cancers.

Autologous Stem Cell and Non-Stem Cell Based Therapies Market Key Players and Their Innovations

Leading companies driving market innovation include:

-

Bristol-Myers Squibb: Notable for Breyanzi, a CAR T-cell therapy, bringing new options for large B-cell lymphoma patients.

-

Gilead Sciences: Developer of Abecma, targeting multiple myeloma with immune cell-based therapies.

-

Novartis: Innovating across clinical development, manufacturing, and formulation of personalized cell therapies with a portfolio spanning oncology and other indications.

-

Johnson & Johnson: Engaged in R&D and providing advanced manufacturing and formulation solutions for cell and gene therapies.

-

Caladrius Biosciences: Focused on pioneering autologous cell therapies for various degenerative and autoimmune diseases.

Challenges and Cost Pressures

High costs stemming from complex and patient-specific manufacturing processes, extensive regulatory requirements, and limited scalability hinder wider adoption. Logistical challenges, such as cold chain management and specialized handling, add further expenses. Improving cost efficiency and streamlining production are critical challenges for stakeholders.

Case Study

FDA label expansions for CAR T-cell therapies have eased post-treatment monitoring requirements, enabling broader clinical use beyond early adopters and increasing eligible patient populations from about 20%. This regulatory adaptation serves as a benchmark for improved therapy access and market expansion.

Read Also: Predictive Genetic Counselling Market

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344