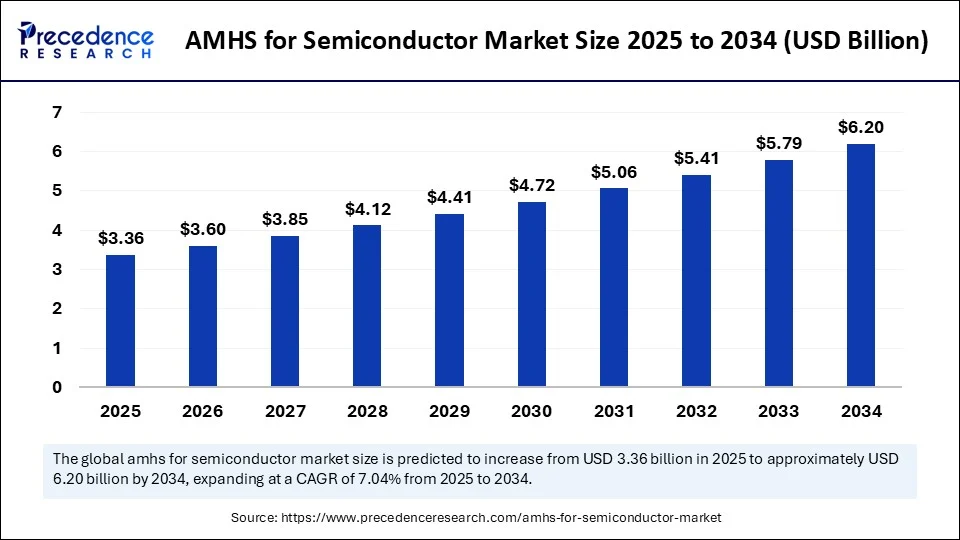

The global Automated Material Handling Systems (AMHS) for semiconductor market is valued at $3.36 billion in 2025 and is expected to hit $6.20 billion by 2034, expanding at a CAGR of 7.04% from 2025 to 2034. Key factors fueling this growth include rising demand for ultra-clean, high-throughput wafer movement driven by the ramp-up of advanced semiconductor nodes and the semiconductor industry’s push for automation and digitalization.

AMHS for Semiconductor Market Quick Insights

-

The global AMHS for semiconductor market size is $3.36 billion in 2025, projected to reach $6.20 billion in 2034.

-

Asia Pacific dominates, holding about 50% revenue share in 2024 and projected at $1.68 billion in 2025 and $3.13 billion in 2034.

-

North America is the fastest-growing region, supported by government investments like the US CHIPS Act and GlobalFoundries expansion.

-

Robotic systems were the largest segment in 2024, with approximately 45% share.

-

Semiconductor fabrication (front-end) accounted for nearly 60% market share in 2024.

-

Wafer handling systems led with about 40% share in 2024.

-

Top players include TSMC, Samsung, Intel, Daifuku, Murata Machinery, SFA Engineering, SK Hynix, SMIC, and more.

Revenue and Segmentation Table

| Year | Global Market Value (USD Billion) | Asia Pacific Market Value (USD Billion) | CAGR (%) (Global) |

|---|---|---|---|

| 2024 | 3.14 | 1.57 | |

| 2025 | 3.36 | 1.68 | 7.04 |

| 2034 | 6.20 | 3.13 | 7.04 |

| Segment | 2024 Share (%) | Key Insight |

|---|---|---|

| Robotic Systems | 45 | Largest component, drives fab automation |

| Semiconductor Fab | 60 | Dominates end-use by handling complex flows |

| Wafer Handling Systems | 40 | Ultra-clean automation in processing |

| On-site Deployment | 70 | Preferred for data security & sync |

| Asia Pacific (Region) | 50 | Largest revenue by region |

How is AI Redefining Fab Automation?

AI integration is transforming AMHS by enabling smarter, adaptive routing for materials, real-time congestion management, and predictive maintenance. Advanced fabs are leveraging AI to optimize complex logistical flows and minimize both downtime and contamination, as manufacturing steps increase and tolerances tighten. AI-driven AMHS platforms are now vital in the shift toward fully automated, “lights-out” fabs—boosting production reliability and throughput beyond levels previously possible with human oversight alone.

AI also helps wafer makers:

-

Analyze real-time sensor data for anomaly detection.

-

Streamline tool-to-tool material transfers with minimal lag.

-

Orchestrate digital twins, optimizing efficiency and pre-emptively resolving bottlenecks.

What’s Driving Market Expansion?

-

Shrinking chip geometries (sub-5nm) and 3D stacking are speeding up fab automation adoption.

-

AI, 5G, and HPC demand are pushing chipmakers to expand advanced, tightly integrated AMHS.

-

Asia Pacific dominance is fueled by major investments from TSMC, Samsung, SK Hynix, and SMIC as well as regional industrial policies in China, Korea, and Taiwan.

-

Robot-equipped, fully automated AMHS are being deployed for 24/7, contamination-free production.

Are Automation and AI Integration the Key to Unlocking Next-Level Fab Competitiveness?

-

Will digital twins and cloud-integrated AMHS enable fabs to continuously optimize in real time?

-

Are smaller and mid-sized fabs able to keep pace given the high cost and complexity, or will this create new competitive barriers?

-

Can global rollouts of government incentives accelerate the democratization of fully automated fabs?

AMHS for Semiconductor Market Regional & Segmentation Overview

-

Asia Pacific: Leads the world, driven by government incentives and the concentration of foundry giants (e.g., TSMC, Samsung, SK Hynix, SMIC). China, Taiwan, South Korea, and Japan see aggressive AMHS rollouts.

-

North America: Fastest anticipated CAGR thanks to the CHIPS Act and corporate investments by GlobalFoundries, Intel, and Texas Instruments.

-

Europe: Innovation led by Germany; focus on supply chain resilience for automotive and 5G.

-

End Users: Front-end fabs dominate; backend packaging/assembly is poised for catch-up growth.

-

By System: Robotic and wafer handling systems enable efficiency jumps in both mature and new fabs.

AMHS for Semiconductor Market Top Companies & Breakthroughs

-

TSMC

-

Samsung Electronics

-

SK Hynix

-

SMIC

-

Intel

-

Daifuku Co. Ltd.

-

Murata Machinery

-

SFA Engineering

-

Texas Instruments

-

GlobalFoundries

-

ASE Group

-

Amkor Technology

-

JCET

Latest Advances:

-

TSMC: Newest AMHS systems in Southern Taiwan Science Park, driving their 2nm fab ramp.

-

GlobalFoundries: $1.5B US CHIPS Act award to expand automated lines.

-

Texas Instruments, Murata, Daifuku: Next-gen robotic systems, digital twins, and energy-efficient modular AMHS lines.

Challenges and Cost Pressures

-

High capital requirements and complex integration are inhibiting uptake by small and medium fabs.

-

Legacy systems can slow the pace of upgrades and complicate transitions to fully automated environments.

-

Ongoing need for specialist support and management of technology transition periods.

Real-World Case: The 2nm Initiative

TSMC’s new 2nm foundry in Taiwan (2024–2025 build) exemplifies how AI-powered AMHS is core to next-generation, high-mix, high-volume production. Digital twin-enabled, the new systems are expected to manage routing, stocker optimization, and flow balancing—unleashing full 24/7 automation in one of the world’s smartest fabs.