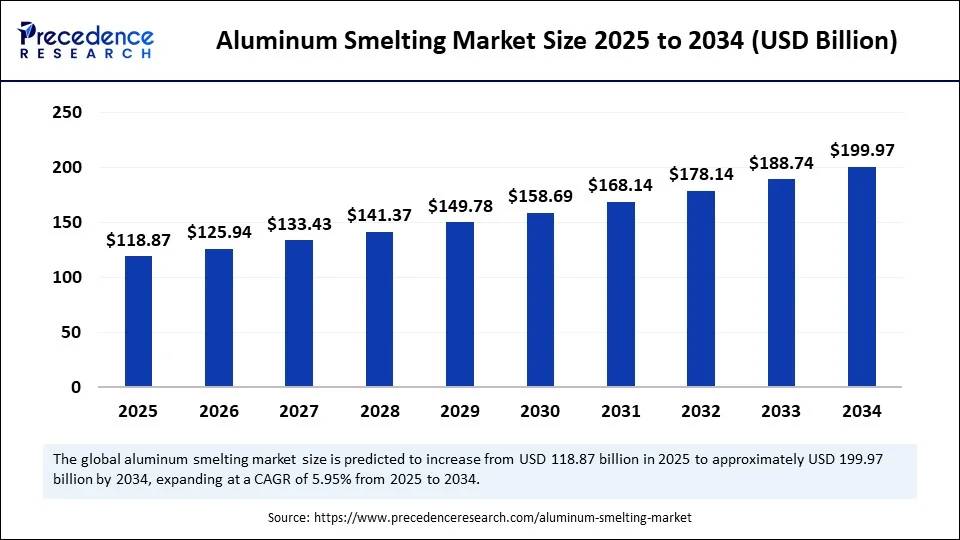

The global aluminum smelting market, valued at $112.19 billion in 2024, is forecast to surge to $199.97 billion by 2034, growing at a CAGR of 5.95%. The market’s upward momentum stems from relentless industrialization, expanding infrastructure investments, and fast-improving smelting processes.

Asia Pacific cements its dominance with over 65% share, led by China’s production might and India’s surging investments.

From fuel-efficient vehicles to skyscrapers and packaging, aluminum’s strength-to-weight ratio and recyclability are propelling its adoption worldwide. The aluminum smelting sector, anchored by the tried-and-tested Hall–Héroult process, but now swiftly integrating greener tech and AI optimization, faces a decade of high demand.

The push for lighter vehicles and aircraft, the advent of electric mobility, and surging construction spend drive both end-user appetite and investment into modernized smelters. Yet, energy costs and carbon emissions loom as core challenges, pushing the industry into its next era of innovation.

Market Highlights

-

In 2024, the market was valued at $112.19 billion, set to reach nearly $200 billion by 2034.

-

CAGR pegged at 5.95% from 2025 to 2034, propelled by automotive and infrastructure growth.

-

Asia Pacific controls 65% of global market share, with China alone housing 60% of world capacity.

-

North America emerges as the fastest-growing region, fueled by EV push and green energy incentives.

-

Hall–Héroult process remains standard, but inert anode technologies rise for carbon-free aluminum.

-

Ingots and billets are the most dominant product forms, feeding automotive, construction, and packaging.

-

Adani Group’s $5 billion investment in India’s smelting sector (December 2024) underlines market vibrancy.

Aluminum Smelting Market Revenue Forecast

| Year | Market Size (USD Billion) |

|---|---|

| 2024 | 112.19 |

| 2025 | 118.87 |

| 2034 | 199.97 |

Artificial intelligence is transforming smelting operations into highly intelligent, energy-optimized systems. By integrating AI-driven production controls, plants have reduced energy usage by up to 17%—a major breakthrough for a historically energy-hungry sector. Machine learning continuously recalibrates process parameters, slashing waste and refining output quality while moving the industry toward sustainability. Cost savings and operational excellence are now more closely aligned than ever before.

AI’s role in aluminum manufacturing doesn’t end with energy efficiency. Data-driven analytics allow companies to predict maintenance needs, track equipment health, and anticipate operational issues before they escalate. As the industry faces mounting pressure for carbon neutrality and lower resource usage, AI will serve as both a compass and an engine for the market’s future resilience and growth.

What Factors Are Powering Market Growth?

-

Industrialization and Urbanization: Explosive regional development, especially in Asia Pacific, catalyzes new infrastructure projects needing lightweight and corrosion-resistant materials.

-

Electric Mobility: EVs and next-gen vehicles demand more aluminum for frames, panels, and power cells, enhancing market reliance on advanced smelter capacity.

-

Government Support: Subsidies and policy initiatives in India, China, and the U.S. help modernize production and shift to low-carbon or renewable-powered smelters.

-

Packaging and Electronics Demand: Growth in lightweight, recyclable packaging and the rapid turnover of consumer electronics drive constant demand spikes across all product forms.

What Opportunities Drive Tomorrow’s Market?

How Do Infrastructure Investments Shape the Next Decade?

Rapid infrastructure programs in both emerging and mature economies open vast new potential for aluminum—across buildings, transport networks, bridges, and electricals. Aluminum’s light weight, durability, and corrosion resistance make it essential for both cutting-edge and practical construction projects. Government and private sector spending, especially in Asia Pacific, is a pivotal catalyst for future demand.

Will Green Smelting Become a Differentiator?

With sustainability fast becoming a competitive edge, companies prioritizing green processes and renewable-powered smelters are set to pull ahead. Inert anode and hydroelectric-powered plants, in particular, are on a steep growth trajectory as global buyers and regulators increasingly demand low-carbon products.

Regional Breakdown: Where the Market Heats Up

Regional Leaders

Asia Pacific: Holds 65% market share and contains the world’s manufacturing giants. China supplies 60% of total smelter output. Nearly a quarter of aluminum here is used in construction, with the region also leading in automotive and electronics consumption.

North America: Fastest growth rate, underpinned by government support, EV adoption, and the rise of hydro-powered smelters. The U.S. claims the largest revenue share in the region thanks to policy moves and investment in renewables and decarbonization.

Market Segmentation

By Process

-

Hall–Héroult Dominance: Continues to be the industry mainstay for high-purity aluminum. Ongoing innovation targets lower energy use and greater integration of renewables.

-

Inert Anode Disruption: Poised for notable growth; eliminates significant CO2 emissions and cuts production costs, heralding a greener future for smelting.

By Power Source

-

Coal Smelters: Still prominent—especially in Asia—but facing growing scrutiny for emissions and costs.

-

Hydroelectric Smelters: Fastest-growing, supported by sustainability goals and often chosen where electricity is expensive, delivering a clear green premium.

By Product Form

-

Ingots: Lead the market with applications in automotive (especially EVs), construction, and aerospace. Billets also accelerate, with demand linked to increased construction and manufacturing.

By Application

-

Automotive & Transportation: Top application, driven by need for lighter, stronger vehicles in the age of fuel economy mandates and EV growth.

-

Electronics: Surge in use for mobile devices, appliances, and consumer electronics as aluminum’s light weight, conductivity, and resistance drive market share.

What’s New: Innovations, Capital, and Key Players

-

Adani Group: Announced a $5 billion investment in aluminum, steel, and copper in December 2024, aiming to boost India’s infrastructure and energy cost competitiveness.

-

Vedanta, Hindalco: Remain top-tier Indian producers expanding capacity and investing in energy integration and greener tech.

-

Product Innovation: Market leaders focus on inert anode technology, green energy integration, and advanced process controls to differentiate in cost and sustainability.

Key Companies

- Nel Hydrogen

- ITM Power

- thyssenkrupp nucera

- Siemens Energy

- McPhy Energy

- Cummins (Hydrogenics)

- Plug Power

- Enapter

- AFC Energy

- Giner ELX (Giner Inc.)

- H2B2 Electrolysis Technologies

- Ohmium International

- Toshiba Energy Systems & Solutions (Toshiba ESS)

- Kawasaki Heavy Industries

- Mitsubishi Heavy Industries (MHI)

- Bloom Energy

- Sunfire

What Are the Main Challenges and Cost Pressures?

Despite record demand, the market faces persistent obstacles.

-

High electricity consumption means operational costs remain volatile; smelters are exceptionally sensitive to electricity price swings.

-

New technologies demand substantial up-front investment, often a barrier for mid-tier and smaller producers.

-

Transitioning to greener smelting not only requires capital but also regulatory and logistical adaptation.

Read Also: Lithium Sulfides Market

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6847

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344