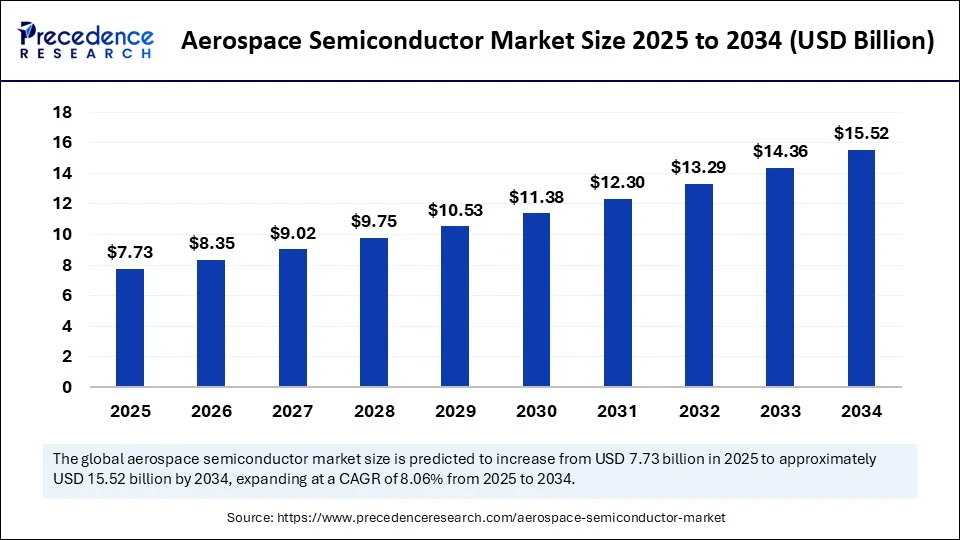

The global aerospace semiconductor market is undergoing a remarkable transformation, valued at USD 7.73 billion in 2025 and forecast to nearly double to USD 15.52 billion by 2034. Buoyed by a robust compound annual growth rate (CAGR) of 8.06% from 2025 to 2034, this sector is primed for extraordinary innovation—from satellites and avionics to AI-powered chip design—with North America holding the dominant share and Asia-Pacific emerging as the next engine for growth.

Aerospace Semiconductor Market Quick Insights

-

The market stands at USD 7.73 billion in 2025, with projections reaching USD 15.52 billion by 2034.

-

CAGR: 8.06% between 2025 and 2034.

-

Top Region: North America, claiming around 40% of the market in 2024 (revenue: USD 2.43 billion in the U.S. alone).

-

Fastest Growth: Asia Pacific, powered by air travel demand and manufacturing expansion.

-

Leading Application: Avionics systems and flight control (over 30% market share in 2024).

-

Top Player Snapshot: Infineon Technologies, NXP Semiconductors, Texas Instruments, Microchip Technology, Broadcom Inc., ON Semiconductor, and more.

-

Commercial Aviation: Dominates with more than 52% market share.

-

Key Materials: Silicon carbide (SiC) and gallium nitride (GaN) for high-temperature, high-reliability applications.

What Is Fueling This Takeoff?

With commercial aviation, defense, and satellite systems demanding smarter, more robust, and energy-efficient electronics, the aerospace semiconductor market is being propelled by:

-

Increased air traffic and fleet expansions worldwide, especially in emerging markets.

-

Government and private sector investments in national security, space exploration, and modernization, especially in North America and China.

-

The push for lighter, more reliable, and energy-saving semiconductor components in avionics, navigation, and propulsion technologies.

AI: The Secret Weapon in Aerospace Chips

Artificial Intelligence is fundamentally reshaping how aerospace-grade semiconductors are conceived, tested, and manufactured. AI-powered design tools accelerate chip innovation, enabling engineers to explore new materials and architectures with unprecedented speed. Machine learning identifies performance patterns and predicts failures, directly improving reliability in high-stakes aerospace environments.

From automating complex simulations to optimizing chip layouts for aerodynamics and resilience under extreme conditions, AI’s influence extends from factory floors to mission-critical applications inside satellites, space vehicles, and next-gen drones. Semiconductors born from this AI-driven ecosystem are smarter, more adaptable, and ready to meet tomorrow’s threats—both on Earth and in orbit.

Aerospace Semiconductor Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 15.52 Billion |

| Market Size in 2025 | USD 7.73 Billion |

| Market Size in 2024 | USD 7.15 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 8.06% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Component Type, Functionality, Platform, Material Type, Technology Node, Appliction, End User, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

What Factors Are Powering Market Growth?

-

Rising Air Traffic: Global demand for air travel and cargo is surging, with the commercial aircraft fleet in Asia-Pacific expected to triple by 2043.

-

Military Modernization: Defense spending is at historic highs, spurring the integration of advanced semiconductors in unmanned systems, surveillance, and navigation.

-

Technological Breakthroughs: Adoption of new materials like SiC/GaN, integration of 5G and IoT technologies, and miniaturization of chips all facilitate safer, more connected, and energy-efficient aerospace systems.

-

Electric and Hybrid Propulsion: The aerospace move toward green propulsion solutions creates new demand for advanced power management semiconductors.

Opportunity and Trend Section: Is Miniaturization the Game Changer?

-

Will the rise of miniaturized, lightweight chips facilitate a new class of autonomous, energy-efficient drones and satellites?

-

Can advances in AI and machine learning unlock the next leap in semiconductor reliability for deep-space missions?

-

Is the shift toward vertical integration and on-shore manufacturing set to offset ongoing supply chain shocks?

Regional and Segmentation Analysis

-

North America: Retains the lead (approx. 40%) due to government investment and deep-rooted aerospace conglomerates like NASA and SpaceX. Its strict safety and quality regimes push semiconductor standards worldwide.

-

Asia Pacific: The fastest-growing region, aided by skyrocketing demand for air travel, aggressive military upgrades, and the world’s biggest semiconductor manufacturing clusters in China, Taiwan, and India.

-

Europe: Focused on high-reliability systems for aviation and space, home to Airbus and satellite system integrators.

-

Latin America, Middle East & Africa: Growing rapidly, spurred by commercial aviation expansion.

By Segment (as per prominent reports):

| Segment | Share/Highlight |

|---|---|

| Integrated Circuits (ICs) | Over 35% market share in 2024 |

| Avionics & Flight Control | Over 30% share |

| Commercial Aviation | Over 52% of total market |

| Technology | Surface-Mount & Through-Hole, focus on miniaturization |

| Application | Communication, Navigation, Imaging, Munitions, Satellites |

Aerospace Semiconductor Market Top Companies and Breakthroughs

-

Infineon Technologies AG: Leading in rad-hard chips for spacecraft.

-

Texas Instruments: Focused on robust analog and mixed-signal devices.

-

Microchip Technology Inc.: Innovating in avionics-grade microcontrollers.

-

Broadcom Inc., NXP Semiconductors, ON Semiconductor: Driving integration, reliability, and next-gen IoT connectivity.

-

Breakthroughs reported: Chips rated for extreme cold, new SiC/GaN modules, and edge-AI enabled avionics processors.

What’s Hindering Market Ascent? Challenges & Pressures

-

Supply Chain Disruptions: Global shocks, geopolitics, and logistics snarls are central risks.

-

Cost Pressures: High R&D and qualification costs for aerospace-grade chips squeeze margins, requiring collaboration and ecosystem resilience.

-

Talent Shortage: The specialized skill set needed hampers pace in R&D and manufacturing.

Case in Point: Smart Defense Readiness

A leading US contractor recently equipped new UAVs with advanced, AI-tuned semiconductor modules capable of real-time threat detection and flight-path optimization under severe electromagnetic interference. This integration slashed mission turnaround times and reduced overall component weight by 22%, directly translating into fuel savings and enhanced range—demonstrating the real-world value proposition for stakeholders mandated to do more with less.

Read Also: Segmented Flow Analyzer (SFA) Market

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026