Hydrogen Internal Combustion Engines Market Key Points

-

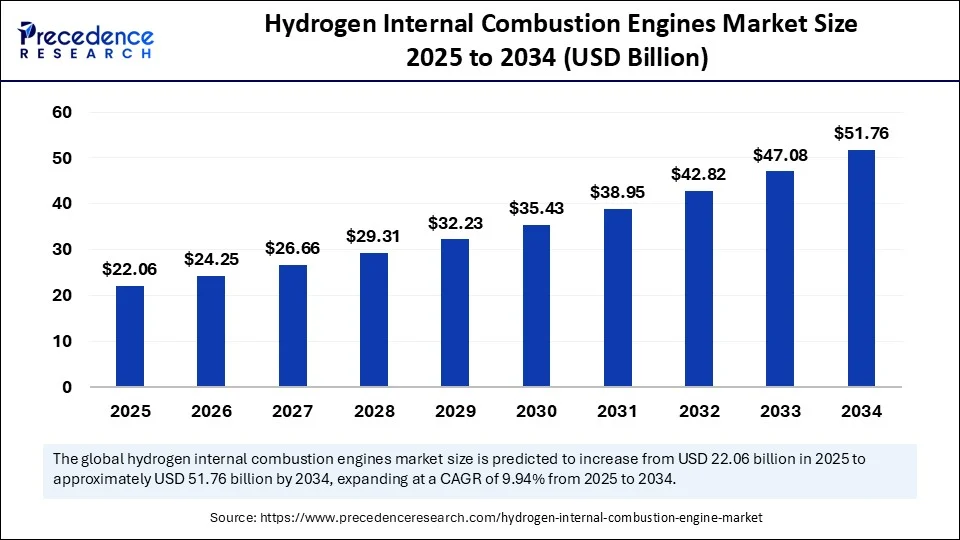

The global hydrogen internal combustion engines market was valued at USD 20.06 billion in 2024 and is projected to reach USD 51.76 billion by 2034, growing at a CAGR of 9.94% from 2025 to 2034.

-

Europe emerged as the leading region, holding 41% of the market share in 2024.

-

The Asia Pacific region is expected to witness the highest growth rate throughout the forecast period.

-

In terms of power output, the 100–300 kW segment led the market with a 43% share in 2024.

-

The 300 kW and above segment is anticipated to grow at the fastest CAGR in the coming years.

-

Among vehicle types, commercial vehicles accounted for the largest share of 49% in 2024.

-

The off-highway vehicles segment is projected to register the most rapid growth during the forecast period.

-

By fuel type, green hydrogen dominated the market with a 56% share in 2024 and is expected to maintain this lead moving forward.

-

Regarding ignition type, the compression ignition with hydrogen-diesel dual-fuel configuration captured the highest share at 38% in 2024.

-

The direct hydrogen injection segment is forecasted to expand at the fastest CAGR from 2025 to 2034.

-

In terms of end-use, the transportation and logistics sector held a significant 46% share of the market in 2024.

-

Meanwhile, the construction and mining industry is projected to be the fastest-growing segment during the forecast period.

Hydrogen Internal Combustion Engines Market Growth Factors

The market is being propelled by several structural growth factors. Firstly, global decarbonization mandates are pressuring industries to find zero-carbon alternatives to diesel, particularly in heavy-duty and off-highway applications. Hydrogen ICEs offer a cost-effective solution by utilizing existing internal combustion engine architecture, reducing the need for extensive retooling.

Secondly, the familiarity of H₂-ICE technology among manufacturers and maintenance crews gives it a competitive edge over fuel cells and electric drivetrains. In addition, growing green hydrogen availability, driven by massive investment in electrolyzer technology, is expected to make hydrogen fuel economically viable in the near future. Finally, prominent OEMs such as Cummins, Tata Motors, MAN, and JCB have accelerated pilot programs and limited production runs, providing strong industrial validation.

Role of AI in the Hydrogen Internal Combustion Engines Market

Artificial intelligence is playing a pivotal role in the evolution of hydrogen ICE technology. During engine development, AI-powered simulations and machine-learning models are used to optimize fuel injection, ignition timing, and combustion parameters, significantly reducing the time and cost of calibration.

In real-time operations, AI enhances engine control systems by dynamically adjusting operating conditions to prevent pre-ignition and knock, both common issues in hydrogen combustion. Predictive maintenance algorithms help monitor wear and performance, scheduling proactive repairs that minimize downtime. AI-driven insights also enable OEMs to design engines that comply with tightening emission standards without compromising power or efficiency.

Market Drivers

Key drivers include the rapid expansion of renewable energy, which creates opportunities for green hydrogen production and storage. Hydrogen ICEs are seen as an efficient means of converting surplus renewable power into dispatchable energy, particularly in remote or mobile applications.

Regulatory pressures on diesel engines—through carbon taxes, bans, and emissions standards—are pushing manufacturers and fleet operators to adopt hydrogen ICEs as a transitional zero-emission solution. Additionally, the logistics and transportation sectors, which face range and weight limitations with battery-electric vehicles, are increasingly turning to hydrogen-powered combustion engines for applications requiring high load capacity and fast refueling.

Opportunities

The market offers substantial opportunities across industries that require heavy-duty, high-utilization equipment. Retrofitting existing diesel engines with hydrogen combustion technology presents a near-term commercial pathway for OEMs and service providers. Hydrogen ICEs also hold promise in mining, construction, and agricultural sectors, where clean but robust power solutions are needed.

Moreover, distributed and backup power applications are beginning to adopt hydrogen gensets, particularly in areas with unstable grids or net-zero targets. Opportunities also exist for component manufacturers, software developers, and AI companies that specialize in combustion optimization, hydrogen fueling systems, and safety technologies.

Challenges

Despite its potential, the hydrogen ICE market faces several challenges. Infrastructure is the most pressing issue—hydrogen production, storage, and distribution remain limited and costly. The volumetric energy density of hydrogen necessitates high-pressure (700 bar) or cryogenic tanks, which add cost and engineering complexity.

Emissions of nitrogen oxides (NOₓ) during hydrogen combustion, while lower than diesel, still require advanced after-treatment systems to meet strict regulations. Safety concerns surrounding hydrogen handling, particularly in public and mobile settings, require robust industry standards and public trust. Additionally, falling battery and fuel cell costs could limit H₂-ICE adoption if hydrogen fueling networks do not scale rapidly.

Hydrogen Internal Combustion Engines Market Regional Outlook

Europe leads the market due to stringent environmental regulations, public funding for hydrogen infrastructure, and large-scale pilot projects. Countries like Germany and the Netherlands are developing hydrogen corridors for freight transportation.

Asia-Pacific is the fastest-growing region, driven by aggressive national hydrogen policies and local manufacturing capacity in countries like China, Japan, India, and South Korea.

North America is showing increasing interest, particularly in California and Canada, where clean fuel mandates and pilot programs are supporting growth.

Latin America is beginning to explore hydrogen ICEs in mining and shipping sectors, while the Middle East and Africa are investing in hydrogen production for export and local industrial use, supporting potential applications in power and transport.

Hydrogen Internal Combustion Engines Market Segmental Insights

-

By Power Output: The 100–300 kW segment led the market in 2024, primarily serving medium-duty transport and commercial applications. Engines above 300 kW are gaining traction in heavy-duty, off-road, and marine sectors.

-

By Vehicle Type: Commercial on-road vehicles, including delivery trucks and freight haulers, dominated the market. Off-highway vehicles, such as those used in mining, construction, and agriculture, are expected to show the fastest growth.

-

By Fuel Source: Green hydrogen accounted for the majority share, supported by rising investments in electrolysis. Blue and grey hydrogen are also in use as transitional fuels in areas with access to natural gas infrastructure.

-

By Ignition Strategy: Compression ignition (dual-fuel hydrogen-diesel systems) holds the largest market share today due to its compatibility with diesel platforms. However, direct hydrogen injection systems are gaining ground as component technologies mature.

-

By End-Use Industry: The transportation sector remains the largest end-use market, but other sectors such as construction, mining, and distributed power are emerging rapidly due to the need for clean, reliable, and heavy-duty energy solutions.

Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 51.76 Billion |

| Market Size in 2025 | USD 22.06 Billion |

| Market Size in 2024 | USD 20.06 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 9.94% |

| Dominating Region | Europe |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Power Output, Vehicle Type, Fuel Type, Ignition Type, End Use Industry, Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Hydrogen Internal Combustion Engines Market Companies

- Cummins Inc.

- Rolls-Royce plc (MTU Engines)

- Toyota Motor Corporation

- MAN Truck & Bus (Volkswagen Group)

- Deutz AG

- Yamaha Motor Co., Ltd.

- Caterpillar Inc.

- JCB

- Hyundai Motor Company

- Punch Hydrocells (Belgium)

Also Read: Cyclic Olefin Polymer Market

You can place an order or ask any questions, please feel free to contact at [email protected]|+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026