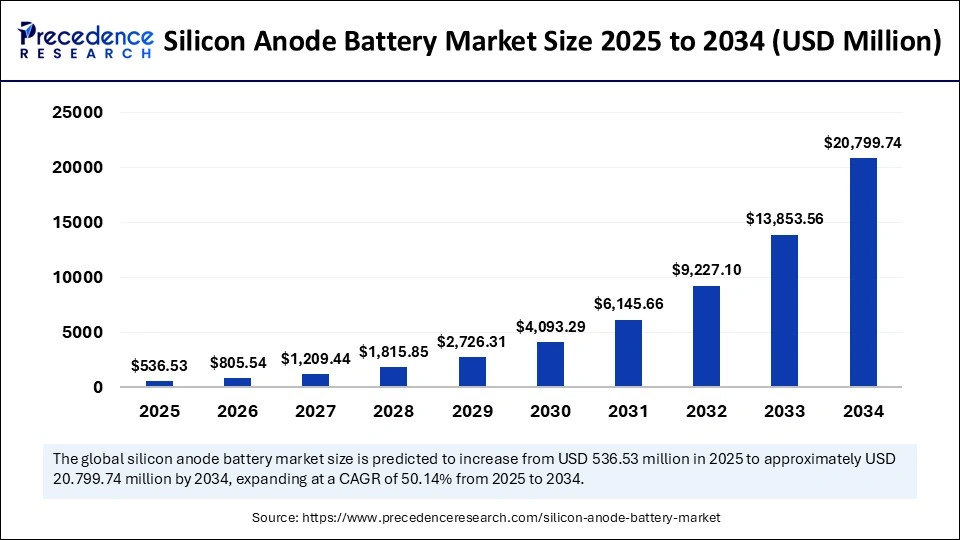

The global silicon anode battery market size is estimated to reach around USD 20,799.74 million by 2034 from USD 357.35 million in 2024, with a CAGR of 50.14%.

Silicon Anode Battery Market Key Insights

-

Asia Pacific dominated the global market with the largest revenue share of 54% in 2024.

-

North America is projected to expand at the fastest CAGR during the forecast period.

-

By capacity, the <1,500 mAh segment captured the biggest market share of 47% in 2024.

-

The 1,500 to 2,500 mAh segment is expected to grow at the fastest CAGR in the coming years.

-

By application, the automotive segment contributed the largest revenue share of 38% in 2024.

-

The energy & power segment is anticipated to grow at a significant CAGR during the forecast period.

Silicon Anode Battery Overview

Silicon anode batteries are advanced lithium-ion batteries that use silicon instead of traditional graphite in the anode (negative electrode). Silicon can store up to 10 times more lithium ions than graphite, which significantly increases the battery’s energy density. This innovation has the potential to drastically improve battery performance in terms of range, charging speed, and lifespan—making it particularly attractive for electric vehicles (EVs), smartphones, and wearable devices.

Advantages and Challenges

The main advantage of silicon anode batteries is their superior capacity and fast-charging potential. However, silicon expands and contracts during charging cycles, which can lead to material degradation and reduced battery life. To overcome this, researchers are developing advanced materials like silicon nanowires and silicon-carbon composites. As technology matures, silicon anode batteries are expected to play a crucial role in next-generation energy storage solutions, supporting the global shift toward electrification and more efficient mobile technology.

How is AI Accelerating Innovation in the Silicon Anode Battery Market?

AI is revolutionizing the silicon anode battery market by streamlining material discovery, optimizing electrode design, and enhancing manufacturing precision. Machine learning models simulate and analyze thousands of material combinations and nanostructures, helping researchers identify optimal designs that improve battery capacity and stability. This accelerates R&D cycles and leads to the development of silicon anodes with significantly higher energy storage potential, overcoming challenges such as volume expansion and material degradation.

AI also plays a critical role in improving production efficiency and product quality. Automated manufacturing processes integrated with AI-powered vision systems can detect defects and ensure uniformity in electrode fabrication. Additionally, AI-driven adaptive charging algorithms help minimize degradation during use by customizing charging profiles based on real-time battery conditions. These innovations not only extend battery lifespan but also enhance the commercial viability of silicon anode batteries for electric vehicles, portable electronics, and grid-scale energy storage.

Growth Factors of the Silicon Anode Battery Market

Surging EV Demand and Clean-Energy Initiatives

The rapid growth of electric vehicles (EVs) and global efforts to reduce carbon emissions are major drivers for silicon anode battery adoption. Silicon anodes offer significantly higher energy density—up to ten times that of graphite enabling longer EV range and faster charging times, making them highly attractive to automakers aiming to meet consumer expectations and regulatory targets. Governments in regions like the U.S., Europe, and Asia-Pacific are supporting clean energy transitions through incentives and funding, accelerating research and commercial implementation of silicon-anode chemistries.

Advances in Nanostructuring and Manufacturing Scale-Up

Material science breakthroughs in nanostructuring—such as nano-silicon powders, silicon-carbon composites, and innovative scaffolds—have significantly mitigated the challenges of silicon swelling and limited cycle life. These innovations improve electrode durability and performance, supporting commercialization across applications from consumer electronics to grid storage. Concurrently, growing R&D investments, strategic partnerships among startups and established firms, and expansion of gigafactory-scale production capacities—especially in North America, China, Japan, and India—are enabling faster market penetration.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6173

Market Schope

| Report Coverage | Details |

| Market Size by 2034 | USD 20,799.74 Million |

| Market Size in 2025 | USD 536.53 Million |

| Market Size in 2024 | USD 357.35 Million |

| Market Growth Rate from 2025 to 2034 | CAGR of 50.14% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | North America |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Capacity, Application, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Dynamics

Market Drivers

The silicon anode battery market is gaining significant momentum, primarily driven by the growing demand for high-performance energy storage solutions across consumer electronics, electric vehicles (EVs), and renewable energy systems.

Compared to conventional graphite anodes, silicon offers up to ten times higher theoretical capacity, significantly enhancing energy density and battery life. As the global push for electric mobility intensifies, EV manufacturers are aggressively seeking battery technologies that provide longer driving ranges, faster charging, and improved efficiency—objectives that silicon anodes are well-suited to meet.

Additionally, rising investments in battery R&D by major automakers and tech companies, along with government incentives for clean energy initiatives, are further accelerating the development and commercialization of silicon-based battery technologies. The growing adoption of wearable devices, smartphones, and laptops also contributes to the demand for compact, lightweight batteries with higher power output.

Opportunities

Silicon anode batteries present vast opportunities in revolutionizing energy storage systems. The EV sector is the most promising segment, where demand for high-capacity, lightweight, and fast-charging batteries is rapidly increasing. As silicon anodes help improve battery performance without fundamentally altering existing lithium-ion cell structures, they offer a relatively seamless integration path for manufacturers.

Another emerging opportunity lies in grid storage for renewable energy sources like solar and wind, where high-capacity batteries can help stabilize energy supply and reduce reliance on fossil fuels. The development of solid-state batteries incorporating silicon anodes also holds transformative potential, offering improved safety and energy density.

Moreover, ongoing advancements in nanotechnology, such as silicon nanowires, graphene coatings, and polymer composites, are enhancing silicon’s stability and cycle life, opening new doors for commercialization in previously constrained applications.

Challenges

Despite its potential, the silicon anode battery market faces several technical and commercial challenges. The biggest hurdle lies in the inherent material properties of silicon, which undergoes significant volumetric expansion (up to 300%) during charge-discharge cycles, leading to structural degradation, reduced cycle life, and loss of electrical contact. This issue necessitates complex engineering solutions such as advanced binders, surface coatings, or hybrid anode designs with graphite blends, which can increase production costs. Manufacturing scalability remains a concern, as the fabrication of high-purity silicon anodes and integration into existing production lines require substantial capital investment and technical expertise.

Moreover, the competitive landscape is dominated by well-established lithium-ion technologies, making market entry difficult for new players unless they can offer substantial performance advantages. Regulatory and safety certifications, especially in EV applications, further slow down the adoption process.

Regional Outlook

North America, particularly the United States, is a leading region in the silicon anode battery market due to the strong presence of tech giants, EV manufacturers, and battery innovators. Government support for advanced battery research and the rise of domestic battery supply chains further contribute to regional leadership. Europe follows closely, driven by aggressive carbon neutrality goals, a booming EV market, and supportive funding from the European Union for battery innovation. Countries like Germany, France, and Sweden are investing heavily in next-gen battery technologies.

Asia-Pacific is poised for the fastest growth, led by countries such as China, Japan, and South Korea, which have well-established battery manufacturing ecosystems and are home to major players like LG Energy Solution, Panasonic, and CATL. China, in particular, is investing in silicon battery R&D to maintain its dominance in EV and battery exports. Meanwhile, regions like Latin America and the Middle East & Africa are still in the early stages of adoption, although growing interest in renewable energy projects may spur future demand for high-capacity batteries in those markets.

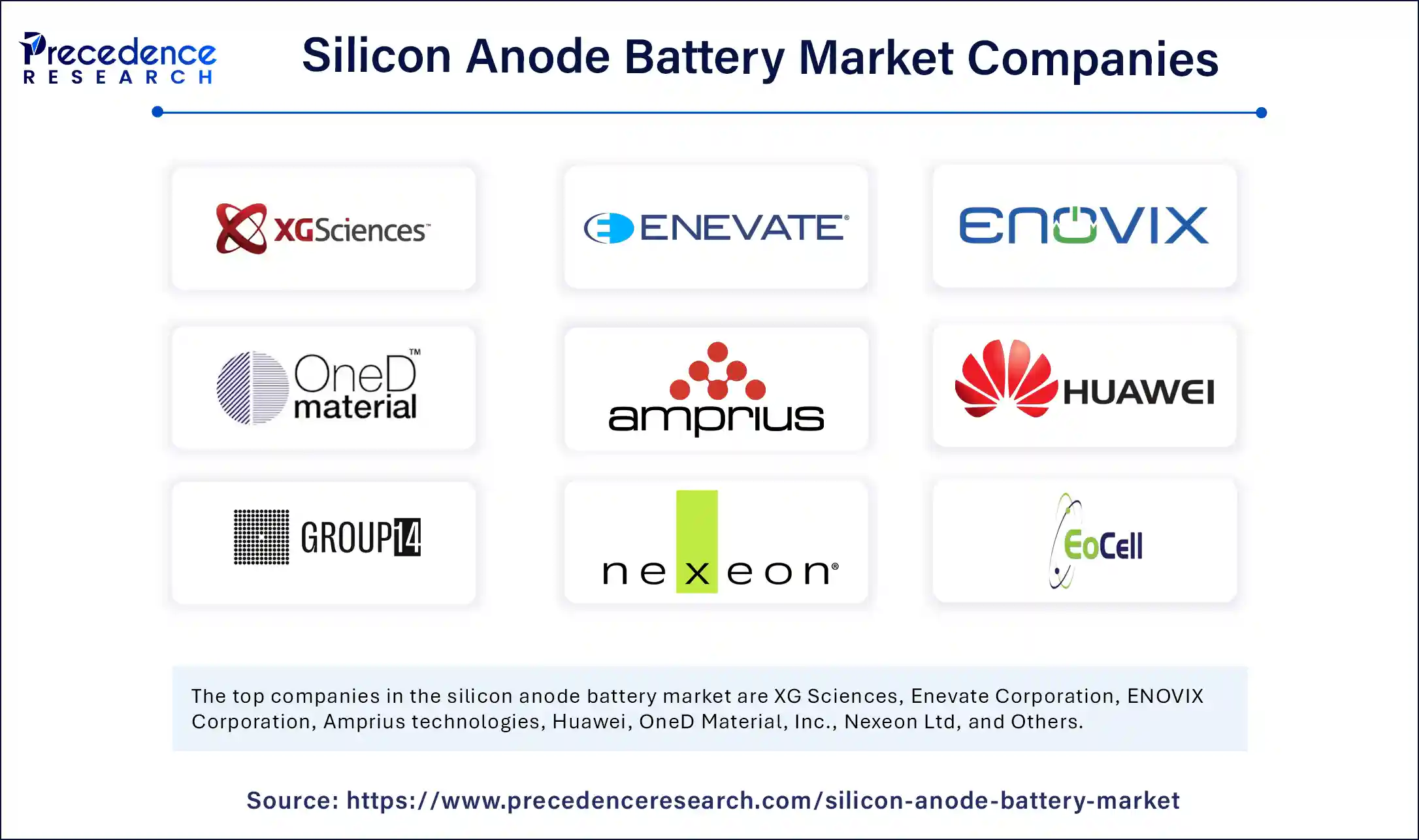

Silicon Anode Battery Market Companies

XG Sciences

Developed silicon-graphene anode materials that enhance battery life and energy density, achieving up to four times the capacity of conventional anodes. Their technology has contributed to improved cycle life, first cycle efficiency, and reduced swelling. Although XG Sciences’ operations have ceased, their technology continues to influence the market through further development by other companies.

Enevate Corporation

Focuses on silicon-dominant anode batteries that enable ultra-fast charging and high energy density, primarily targeting the electric vehicle (EV) market. Enevate’s technology is recognized for reducing charging times and increasing the driving range of EVs.

ENOVIX Corporation

Designs next-generation silicon-anode lithium-ion batteries for portable electronics and wearables. ENOVIX products are known for improved energy capacity, safety, and longevity in small form-factor devices.

Amprius Technologies

Leads in the development of silicon nanowire anode batteries, delivering high energy density and rapid charging capabilities. Their batteries are used in drones, aerospace, and electric vehicles, offering lightweight solutions with extended range.

Huawei

Develops silicon anode battery technology to enhance battery life and charging speed in smartphones and mobile devices. Huawei’s advancements aim to deliver longer-lasting and faster-charging consumer electronics.

OneD Material, Inc.

Specializes in silicon nanowire anodes compatible with existing battery manufacturing processes. The company targets the EV and high-performance battery markets, aiming to improve energy density and manufacturability.

Nexeon Ltd

Produces engineered silicon materials for battery anodes and partners with battery and automotive companies to improve EV battery performance. Nexeon’s materials are designed to increase energy density and cycle life in automotive applications.

California Lithium Battery

Works on silicon-graphene composite anodes to boost energy density and lifespan, targeting electric vehicles, grid storage, and portable electronics. Their focus is on extending battery life and supporting high-capacity applications.

EoCell Inc.

Develops high-capacity silicon anode batteries aimed at electric vehicles and renewable energy storage. EoCell emphasizes cost-effective innovation and scalability for large-scale battery applications.

Group14 Technologies

Provides silicon-carbon composite anode materials that enhance energy density and charging speed for electric vehicles and consumer electronics. Group14’s technology is designed to be easily integrated into current battery manufacturing lines.

Segments Covered in the Report

By Capacity

- <1,500 mAh

- 1,500 to 2,500 mAh

- >2,500 mAh

By Application

- Automotive

- Consumer Electronics

- Energy & Power

- Medical Devices

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Also Read: Intelligent Battery Sensor Market

You can place an order or ask any questions, please feel free to contact at [email protected]|+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026