Market Expansion Driven by Energy Efficiency, Technological Innovation, and Sustainability Trends

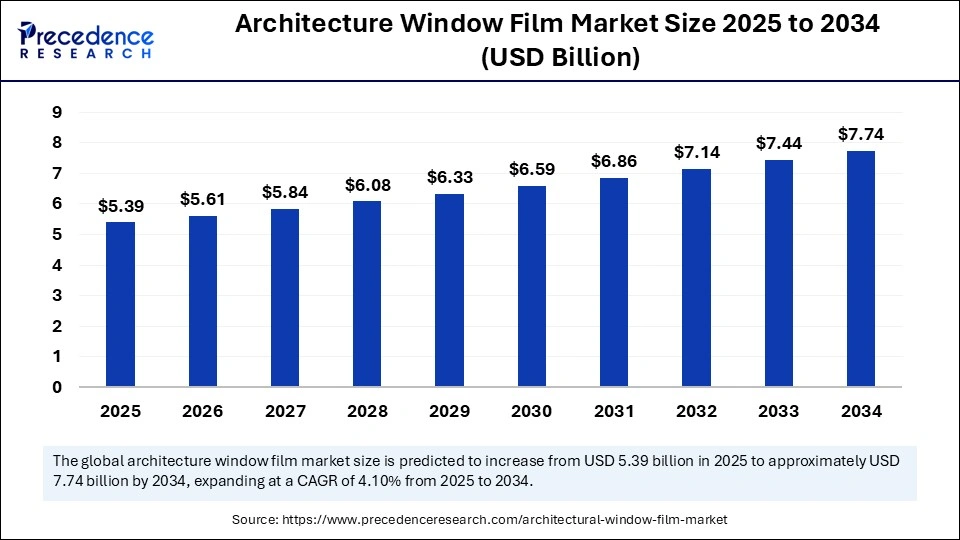

The global architectural window film market is poised for solid growth, with valuations expected to rise from USD 5.39 billion in 2025 to approximately USD 7.74 billion by 2034. This represents a compound annual growth rate (CAGR) of 4.10% over the forecast period from 2025 to 2034. The accelerating demand is fueled primarily by the growing need for energy-efficient building solutions, enhanced occupant comfort, and increased adoption of sustainable construction practices.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7069

Introduction: What Is Propelling the Architectural Window Film Market?

The market for architectural window films is gaining momentum as building owners, developers, and design professionals increasingly recognize the benefits of window films in reducing energy consumption, blocking harmful UV radiation, and improving visual comfort. Rising energy costs and stringent government regulations promoting green building initiatives are key catalysts for market growth.

Additionally, rapid urbanization, particularly across Asia Pacific, is boosting demand across commercial and residential sectors. This trend is further supported by technological innovations such as smart films that adapt dynamically to light and heat conditions.

Architectural Window Film Market Key Points

-

The market size stood at USD 5.39 billion in 2025 and is projected to reach USD 7.74 billion by 2034.

-

Asia Pacific leads the market with a 40% share in 2024, driven by rapid urbanization and construction activity.

-

North America is the fastest-growing region, spurred by sustainable building regulations and retrofitting demand.

-

Solar control films, particularly metalized types, held the largest product segment share at 30% in 2024.

-

Major industry participants include Eastman Chemical Company, 3M Company, Saint Gobain, and Johnson Window Films.

-

Commercial buildings dominate application due to their high energy costs and regulatory requirements.

-

The market features wide segmentation by product type, application, material, and regional distribution.

Market Revenue Breakdown (USD Billion)

| Year | Market Size (USD Billion) |

|---|---|

| 2025 | 5.39 |

| 2026 | 5.61 |

| 2030 | 6.70 |

| 2034 | 7.74 |

Artificial Intelligence (AI) is transforming the architectural window film landscape by enabling the development of smart films and advanced manufacturing techniques. AI-powered smart films can dynamically adjust their tint and opacity based on real-time environmental conditions, optimizing daylight and thermal control while enhancing occupant comfort. Integration with building management systems (BMS) allows for automated control through sensors and voice commands, making window films smarter and more responsive.

On the manufacturing front, AI streamlines production processes by improving quality control through defect and inconsistency detection. It also enables customization and innovation in film formulations, ensuring superior optical and thermal properties. The use of AI ensures higher product reliability, reduces waste, and supports the growing demand for next-generation energy-efficient architectural solutions.

What Are the Key Factors Driving Market Growth?

-

Increasing demand for energy-efficient building materials to reduce heating and cooling costs.

-

Rising awareness about UV protection and glare reduction for occupant health and comfort.

-

Rapid urbanization and large-scale construction projects, notably in Asia Pacific.

-

Technological advancements including spectrally selective films, nanoceramic coatings, and smart films.

-

Government incentives, green certifications, and stricter building codes promoting energy conservation.

-

Growing retrofitting activities in older buildings to meet modern sustainability standards.

-

Expanding applications in commercial (offices, hospitals, retail) and residential sectors.

What Market Opportunities and Trends Are Emerging?

Are smart and sustainable films gaining traction?

The rise of smart window films with adaptive light and heat control capabilities is a significant trend, combining sustainability with enhanced building management integration.

How is retrofitting driving demand?

Retrofitting existing buildings with window films offers a cost-effective alternative to full window replacement while achieving energy savings and improved comfort, creating vast market opportunities in mature regions like North America and Europe.

Are decorative and privacy films expanding their footprint?

The growing interior design focus in both commercial and residential spaces is increasing the adoption of decorative and privacy films, broadening market applications beyond functionality.

Regional and Segment Analysis

Asia Pacific dominates with approximately 40% market share due to urbanization, energy-conscious infrastructure projects, and solar control needs for hot climates. The region’s market valuation is projected to grow from USD 2.16 billion in 2025 to USD 3.13 billion by 2034, at a CAGR of 4.22%.

North America stands out as the fastest-growing region, driven by growing green building certifications, retrofit programs, and proficiency in advanced smart films. European markets also show steady growth with stringent energy regulations.

Segment-wise, metalized solar control films lead the product category with a 30% share, primarily adopted in commercial buildings which dominate end-use. Residential applications are rapidly expanding, driven by consumer demand for sustainable and aesthetic window solutions. The functionality segments like energy/heat reduction films hold significant market importance.

What Are the Latest Breakthroughs from Leading Companies?

Market leaders such as Eastman Chemical Company (with brands like LLumar® and SunTek®), 3M Company (3M™ Window Films), and Saint-Gobain Solar Gard are innovating aggressively. Eastman notably introduced advanced solar control and nanoceramic films known for high-performance heat rejection and UV protection. 3M leverages nanotechnology and multi-layer optical innovations for enhanced film durability and aesthetics.

Additionally, Johnson Window Films and other key players are advancing smart film technologies that dynamically adapt to environmental conditions, integrating with IoT for intelligent building management.

Key Players in the Market

-

Eastman Chemical Company (LLumar®, SunTek®)

-

3M Company (3M™ Window Films)

-

Saint-Gobain (Solar Gard)

-

Johnson Window Films

-

Avery Dennison Corporation

-

Garware Suncontrol

-

Lintec Corporation

-

Polytronix Inc

-

Purlfrost Ltd

-

Armolan

What Challenges and Cost Pressures Does the Market Face?

High initial investment costs for advanced films like nanoceramic and smart films can deter adoption, especially in price-sensitive residential projects and developing economies. Although long-term energy savings are substantial, upfront costs remain a barrier.

Other challenges include the durability of lower-quality films under harsh weather, competition from alternative technologies such as smart glass, and the need for skilled installation to ensure optimal performance.

Case Study: Energy Savings in Commercial Retrofitting

A large commercial office building in a hot climate region implemented metalized solar control window films on its glass facade. The retrofit reduced cooling energy consumption by 15%, decreasing HVAC load and delivering annual cost savings of approximately 10%. Improved occupant comfort and reduction in glare also enhanced tenant satisfaction. This case exemplifies the increasing viability of window films as cost-effective energy management solutions for commercial real estate.

Architecture Window Film Market Segments Covered in the Report

By Product Type

- Solar Control Films – Dyed

- Solar Control Films – Metalized

- Solar Control Films – Nano-Ceramic

- Safety & Security Films

- Decorative & Privacy Films

- Anti-Graffiti Films

- UV-Protection Films

- Insulating / Low-E Films

- Smart / Switchable Films (PDLC, SPD, Electrochromic)

- Specialty Films (Acoustic, Anti-Fog, Self-Cleaning)

By Application

- Residential Buildings

- Commercial Buildings (Offices, Retail, Mixed-Use)

- Hospitality (Hotels, Resorts)

- Healthcare (Hospitals, Clinics)

- Education & Institutional (Schools, Universities, Government)

- Industrial & Warehousing

- Cultural & Heritage Spaces (Museums, Galleries)

By Functionality

- Energy / Heat Reduction

- Security & Safety

- Privacy & Aesthetics

- UV & Fade Protection

- Thermal Insulation (Low-E)

- Smart Light/Privacy Control

- Anti-Graffiti & Maintenance Protection

By Material / Construction

- Polyester (PET) Films

- Metalized Films

- Ceramic / Nano-Ceramic Films

- Laminated Multi-Layer Films

- Electroactive Films (PDLC, SPD, Electrochromic)

By Thickness

- Thin Films (<50 µm)

- Medium Films (50–150 µm)

- Thick Films (>150 µm)

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Read Also: Gas Insulated Substation Market

You can place an order or ask any questions. Please feel free to contact us at [email protected] |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Company Ecosystem and Revenue Overview - May 20, 2026

- ESG Software Market Surges Toward USD 31.96 Billion by 2035 as AI-Powered Compliance and Sustainability Reporting Transform Global Enterprises - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Surges Toward USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026