Accelerated by AI, 5G, and Automotive Innovation, Global Market to Surge at 8.06% CAGR with Asia Pacific Leading the Charge

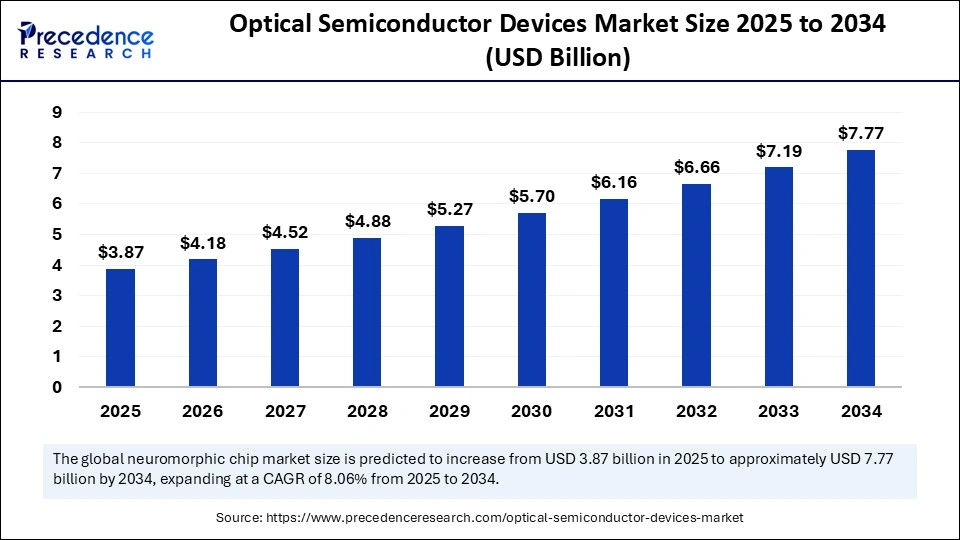

The global optical semiconductor devices market has reached a pivotal moment, valued at USD 3.87 billion in 2025 and projected to catapult to USD 7.77 billion by 2034, displaying a robust CAGR of 8.06% over the forecast period.

The sector’s stellar momentum is being shaped by rising demand for high-speed data transfer, advanced sensing, and energy-efficient solutions servicing the telecommunication, automotive, industrial, and medical sectors. Fundamental drivers include the expansion of data centers, rapid 5G deployments, the proliferation of autonomous vehicles, and the explosion of IoT connectivity.

Optical Semiconductor Devices Market Key Highlights

-

The market value is USD 3.87 billion in 2025, growing to USD 7.77 billion by 2034.

-

Asia Pacific remains the dominant region, with North America projected as the fastest growing.

-

Light Emitting Diodes (LEDs) lead segment share due to energy efficiency and versatility.

-

In 2024, global LED production surpassed 91 billion units; over 10 billion image sensors shipped.

-

Automotive innovation: 85% of new vehicles in developed markets now feature optical sensors such as LiDAR.

-

Leading players like Samsung, SK Hynix, and TSMC spearhead market breakthroughs.

Optical Semiconductor Devices Market Revenue Table

| Year | Market Size (USD Billion) |

|---|---|

| 2024 | 3.58 |

| 2025 | 3.87 |

| 2034 | 7.77 |

Regional Spotlight: Asia Pacific’s Market Supremacy

Asia Pacific exhibited market dominance in 2024, with USD 1.47 billion in revenues and a projected leap to USD 3.22 billion by 2034 at 8.16% CAGR. The region’s leadership stems from a powerful electronics manufacturing base, extensive consumer markets, and government incentives fueling 5G infrastructure—with over 3.8 million 5G base stations already operational.

AI’s Transformative Role in the Market

Artificial intelligence (AI) is rewriting the playbook for optical semiconductor device manufacturing and innovation. AI algorithms enable smarter, more efficient fabrication by optimizing design, reducing waste, and predicting faults, leading to substantial cost reductions and shorter development cycles. Importantly, AI-driven workloads require new hardware optimized for high-bandwidth optical interconnects—driving the need for photonics that outperform traditional electrical connectivity in speed and efficiency.

Beyond production, AI is central to evolving new functionalities in optical devices—from advanced image sensors for facial recognition to real-time data analysis in autonomous vehicles. This strengthens end-use sectors, ensuring that optical semiconductors remain at the heart of next-generation data processing, sensing, and communication technologies.

What’s Driving Optical Semiconductor Market Growth?

Why Is High-Speed Data Transmission a Game-Changer?

The optical semiconductor devices market is energized by escalating demand for high-speed, energy-efficient data transmission. This surge is largely attributed to AI-powered applications, expanded cloud workloads, and the need for fiber-optic communications in data centers and telecom networks. Automotive advancements, especially in electric and self-driving vehicles, further propel the market—optical sensors and laser diodes now form the backbone of safety and navigation systems for advanced driver-assistance functions.

How Do Materials Like GaN and InP Shape the Future?

Gallium Nitride (GaN) and Indium Phosphide (InP) are taking the lead in revolutionizing device performance. GaN enables brighter light output with less energy loss while maintaining compact high-power densities, particularly in LEDs and laser diodes. Meanwhile, InP is earmarked for rapid expansion in 5G and AI-driven applications due to its unique material properties and high-frequency operational capacity.

Opportunity & Trends

What Opportunities Are Created by Integrating Silicon Photonics and AI?

Integration of silicon photonics with AI infrastructure unlocks the door for ultrafast, energy-efficient data processing. The physical limitations of conventional electrical interconnects are being overcome by light-based communication, which slashes energy consumption and supports the scalability of hyperscale data centers—an essential solution for the exponential data growth seen in AI and HPC environments.

Which Segments Are Most Promising for Innovation?

-

Laser Diodes: Poised for fastest CAGR due to their growing use in medical devices, advanced manufacturing, and high-performance sensing for autonomous vehicles and consumer electronics.

-

Integrated Optical Devices: Photonic Integrated Circuits (PICs), embedding multiple components on a chip, are rapidly expanding in IT and telecom thanks to their speed, latency, and efficiency advantages.

Regional Analysis

-

Asia Pacific: Led by China, South Korea, and Japan, the region benefits from an unbeatable manufacturing ecosystem and government support, reinforcing R&D and supply chain dominance.

-

North America: Projected fastest growth, with technology breakthroughs and data center scale driving optical semiconductor demand for advanced computing and 5G networking.

-

Europe: Strength in automotive and telecommunications, leveraging regulatory incentives and mature supply chains for innovation.

Segmentation Analysis

Device Type Breakdown

-

Dominant Segment: LEDs, which excel in energy-efficient lighting and broad utility.

-

Rising Star: Laser diodes, especially for industrial, automotive, and medical use.

Material Analysis

-

Gallium Nitride (GaN): Leading the push into high-performance, compact, and efficient solutions for optoelectronics.

-

Indium Phosphide (InP): Fastest growth potential for advanced network infrastructure and smart devices.

Application Segmentation

-

Telecommunications & Data Centers: Lead the market by volume, reflecting insatiable demand for high-speed, reliable connectivity.

-

Automotive: The fastest expansion, with ADAS, electric vehicles, and LiDAR sensors providing multi-dimensional sensing power.

Integration Technology

-

Discrete Optical Devices: Preferred for high-power, robust environments.

-

Photonic Integrated Circuits (PICs): Key to next-generation connectivity and miniaturization.

Top Companies in the Optical Semiconductor Devices Market

Tier I – Major Players

These dominant companies individually hold significant market shares and together contribute roughly 40–50% of the total market revenue.

- Broadcom Inc.: A global leader in semiconductor and infrastructure software, Broadcom offers high-performance optical components widely used in data centers and telecommunications.

- ams OSRAM Group: Known for its expertise in optical solutions, ams OSRAM specializes in advanced light emitters, sensors, and laser technologies for automotive and industrial applications.

- ROHM Semiconductor: ROHM provides a broad portfolio of optoelectronic components, including laser diodes and optical sensors, focused on automotive and consumer electronics sectors.

- Coherent Inc.: Coherent is a major supplier of lasers and optical components used in semiconductor manufacturing, medical devices, and defense technologies.

- Lite-On Technology Corp.: Lite-On is a key player in optoelectronics, producing LEDs, optical sensors, and photodetectors for mobile devices, automotive systems, and industrial applications.

Tier II – Mid-Level Contributors

These firms have strong market presence but less dominance than Tier I players, collectively contributing about 30–35% of the market.

- Nokia (including Infinera)

- Infineon Technologies

- STMicroelectronics

- Skyworks Solutions

Tier III – Niche and Regional Players

Smaller or regionally focused companies with modest individual contributions, but collectively accounting for around 15–20% of the market.

- Hamamatsu Photonics

- Nichia Corporation

- Vishay Intertechnology

- Toshiba Corporation

- Akasaki Microelectronics

Recent Advancements

- In September 2025, POET Technologies Inc. and Semtech Corporation began customer sampling of their high-performance 1.6T Receiver Optical Engines tailored for AI and cloud networks. These engines leverage POET’s Optical Interposer™ platform combined with Semtech’s 200G-per-lane receiver technology, featuring DR8 for short-reach AI links and 2×FR4 for extended intra-data center connectivity.

- In the same month, Coherent Corp. unveiled a new series of quad-channel integrated circuits aimed at boosting optical transceiver speeds in cloud and telecom networks. The lineup includes a 4-channel driver for silicon photonics Mach-Zehnder modulators supporting 800G and 1.6T modules, as well as a chipset for 400G coherent links. These solutions are engineered for lower power consumption and feature integrated monitoring capabilities.

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/6952

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344